What do you mean by S Corp shareholder distributions?

Ava Robinson

Published Feb 24, 2026

S Corp Shareholder Distributions: Everything to Know. S corp shareholder distributions are the earnings by S corporations that are paid out or “passed through” as dividends to shareholders and only taxed at the shareholder level.

How often does A S corporation make a profit?

Profit Distributions. An S corporation can distribute allocated profits once a year or at any regular interval. The board of directors must vote and pass a resolution to distribute profits, setting the date for the distributions. Typically, distributions are authorized in quarterly, bi-annual or annual payments.

Can A S corporation make a tax free distribution?

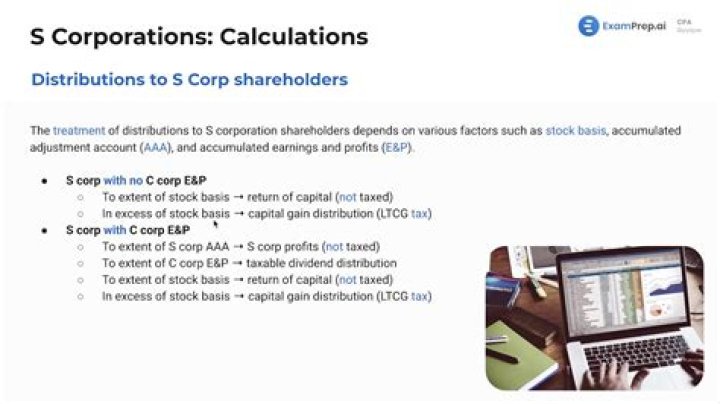

Subsequent distributions by the S corporation to the shareholders often can be made tax-free. However, the taxation of distributions is more complicated if the S corporation has C corporation accumulated earnings and profits (E&P).

What happens if you mishandle a s Corp distribution?

Mishandling distributions can result in the IRS terminating the S corporation’s favorable tax status, which can have dire tax consequences for the corporation and its shareholders.

When does a corporation want to remove a shareholder?

When a corporation wishes to remove a shareholder from a business, there are several particular steps that they must follow. These steps are determined by the nature of the relationship between the business and the shareholder and the corporate documents.

Can a board of directors force out a shareholder?

Otherwise, you cannot force out a shareholder until they have violated the corporate statute. In most cases, this would mean that the shareholder has committed fraud. After everything is in order, your corporate secretary and board of directors should sign the removal resolution.

Can a shareholder ask for a business to be dissolved?

Under this second cause of action, if a shareholder or group of shareholders owns enough of the business’ stock, they can ask that the business be dissolved. This request is made on the allegation that the majority is committing unfair practices that unduly and financially burden minority shareholders.

How are property distributions treated in a S corporation?

Property Distributions Property distributions from an S corporation are treated like those from a C corporation, in that if the fair market value (FMV) exceeds the corporation’s tax basis, then the corporation must recognize the gain as if it sold the property to the shareholder.

How is an S corporation different from a partnership?

Unlike a partnership, an S corporation is not subject to personal holding company tax or accumulated earnings tax. When income is earned by an S corporation, it is taxed only once, regardless of whether the income is distributed or invested.

Do you have to pay taxes on S corporation distributions?

General Overview of S Corporation Distributions Unlike a partnership, an S corporation is not subject to personal holding company tax or accumulated earnings tax. When income is earned by an S corporation, it is taxed only once, regardless of whether the income is distributed or invested.

How is money taken out of a S corporation?

S corporation owners may take money out of the corporation in a variety of ways, such as in the form of wages and distributions. Distributions from earnings are not subject income tax withholding. A distribution is made by simply cutting a check for a specific amount, made payable to the shareholder(s).

How are loans to shareholders’s Corp treated?

This way, subsequent debt payments are treated as capital gain instead of regular income and taxed at a lower rate. Another alternative is making the corporation wait to repay the shareholder debt until there is a year with positive net income to restore most or all of the loan basis.

Can a shareholder put money into a corporation?

The shareholder can also put money into the corporation when it needs an infusion of cash, but the corporation has to be diligent in repaying the loan so as to avoid incurring taxes for that shareholder.