What do bond spreads indicate?

Mia Ramsey

Published Feb 16, 2026

The bond spread or yield spread, refers to the difference in the yield on two different bonds or two classes of bonds. Investors use the spread as in indication of the relative pricing or valuation of a bond.

What does it mean when bond spreads widen?

The direction of the spread may increase or widen, meaning the yield difference between the two bonds is increasing, and one sector is performing better than another. Widening spreads typically lead to a positive yield curve, indicating stable economic conditions in the future.

How do you calculate default spread?

Secondly, how do you find the default spread? The cost of debt for a company is then the sum of the riskfree rate and the default spread: Pre-tax cost of debt = Risk free rate + Default spread. The default spread can be estimated from the rating or from a traded bond issued by the company or even a company CDS.

What is a bond spread and how is it related to the default risk premium?

A high-yield bond spread, also known as a credit spread, is the difference in the yield on high-yield bonds and a benchmark bond measure, such as investment-grade or Treasury bonds. High-yield bonds offer higher yields due to default risk. The higher the default risk the higher the interest paid on these bonds.

How are bond ratings related to default risk?

The credit risk or default risk is the risk of an issuer not making timely interest or principal payments as promised. A bond with AA rating is less likely to default than an A rated bond, which is less likely to default than a bond with BBB (triple B) rating, and so on.

What do tightening bond spreads indicate?

The direction of the yield spread can increase, or “widen,” which means that the yield difference between two bonds or sectors is increasing. When spreads narrow, it means the yield difference is decreasing.

What is default spread definition?

The default spread is usually defined as the yield or return differential between long-term BAA corporate bonds and long-term AAA or U.S. Treasury bonds. In fact, as much as 85 percent of the spread can be explained as reward for bearing systematic risk, unrelated to default.

What is default credit spread?

A credit spread is the difference in yield between a U.S. Treasury bond and another debt security of the same maturity but different credit quality. Credit spreads are also referred to as “bond spreads” or “default spreads.” Credit spread allows a comparison between a corporate bond and a risk-free alternative.

How is bond spread calculated?

Subtract the lower interest rate from the higher interest rate. That will be the bond spread. Yield spread can also be calculated between other debt securities, such as certificates of deposit. For example, if one bond has a yield of 5 percent and another has a yield of 4 percent, the spread is 1 percent.

Is a BBB bond rating good?

Bonds with a rating of BBB- (on the Standard & Poor’s and Fitch scale) or Baa3 (on Moody’s) or better are considered “investment-grade.” Bonds with lower ratings are considered “speculative” and often referred to as “high-yield” or “junk” bonds.

Is spread tightening good or bad?

Bond credit spreads are often a good barometer of economic health – widening (bad) and narrowing (good). A credit spread can also refer to an options strategy where a high premium option is written and a low premium option is bought on the same underlying security.

Why do firms default?

Default is often assumed to occur when market assets fall below a certain boundary. Consistent with this hypothesis, some low-value firms default despite sufficient liquidity. How- ever, liquidity shortages can precipitate default at high asset values when firms are restricted from accessing external financing.

What is credit default swap in simple terms?

A credit default swap (CDS) is a financial derivative or contract that allows an investor to “swap” or offset his or her credit risk with that of another investor. To swap the risk of default, the lender buys a CDS from another investor who agrees to reimburse the lender in the case the borrower defaults.

Do credit default swaps still exist?

The payment received is often substantially less than the face value of the loan. Credit default swaps in their current form have existed since the early 1990s, and increased in use in the early 2000s. CDSs are not traded on an exchange and there is no required reporting of transactions to a government agency.

Are bonds subject to default risk?

All bonds carry some degree of “credit risk,” or the risk that the bond issuer may default on one or more payments before the bond reaches maturity. In the event of a default, you may lose some or all of the income you were entitled to, and even some or all of principal amount invested.

One may also ask, how do you find the default spread? The cost of debt for a company is then the sum of the riskfree rate and the default spread: Pre-tax cost of debt = Risk free rate + Default spread. The default spread can be estimated from the rating or from a traded bond issued by the company or even a company CDS.

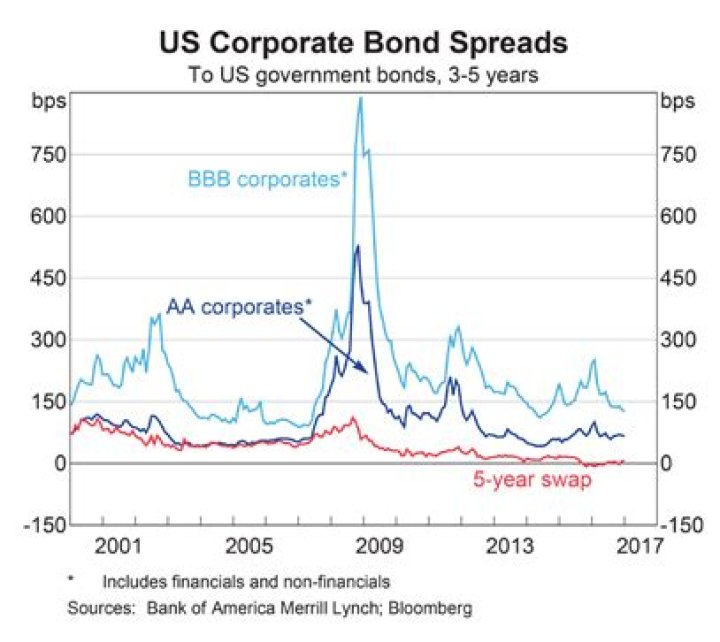

Bond spreads tighten with improving economic conditions and widen with deteriorating economic conditions. You can see evidence of these trends in spreads’ behaviors during the credit crisis of 2008–2009. In terms of business cycles, widening spreads indicate a slowing economy.

What is the default spread?

The default spread is usually defined as the yield or return differential between long-term BAA corporate bonds and long-term AAA or U.S. Treasury bonds. 2 However, as Elton et al. (2001) show, much of the information in the default spread is unrelated to default risk.

How is the default spread of a bond defined?

The term default spread can be defined as the difference between the yields of two bonds with different credit ratings. The default spread of a particular corporate bond is often quoted in relation to the yield on a risk-free bond such as a government bond for similar duration. Furthermore, what is default spread definition?

How are bond spreads related to credit risk?

Relate your bond spread to credit risk. Bond spreads, and particularly credit spreads, are related to the perceived risk of investing in a bond. That is, the risk that the issuer (the foreign entity or corporation that backs the bond) will not make payments on that bond as promised. As the risk increased, the credit spread also increases.

How are default spread and riskfree rate related?

The cost of debt for a company is then the sum of the riskfree rate and the default spread: Pre-tax cost of debt = Risk free rate + Default spread. The default spread can be estimated from the rating or from a traded bond issued by the company or even a company CDS. Similarly one may ask, what is a country default spread?

How to calculate the spread between two bonds?

In its most basic form, a bond spread is simply the difference, or “spread,” between two bond interest rates. Note the interest rate of a given bond, and then select another bond with which to compare it. Note that bond’s interest rate.