What deductions can be used for adjusted gross income?

James Craig

Published Mar 29, 2026

AGI is used to calculate your taxes in two ways: It’s the starting point for calculating your taxable income—that is, the income you pay taxes on. To get taxable income, take your AGI and subtract either the standard deduction or itemized deductions and the qualified business income deduction, if applicable.

How do I calculate my AGI deduction?

Here’s how you work out your AGI:

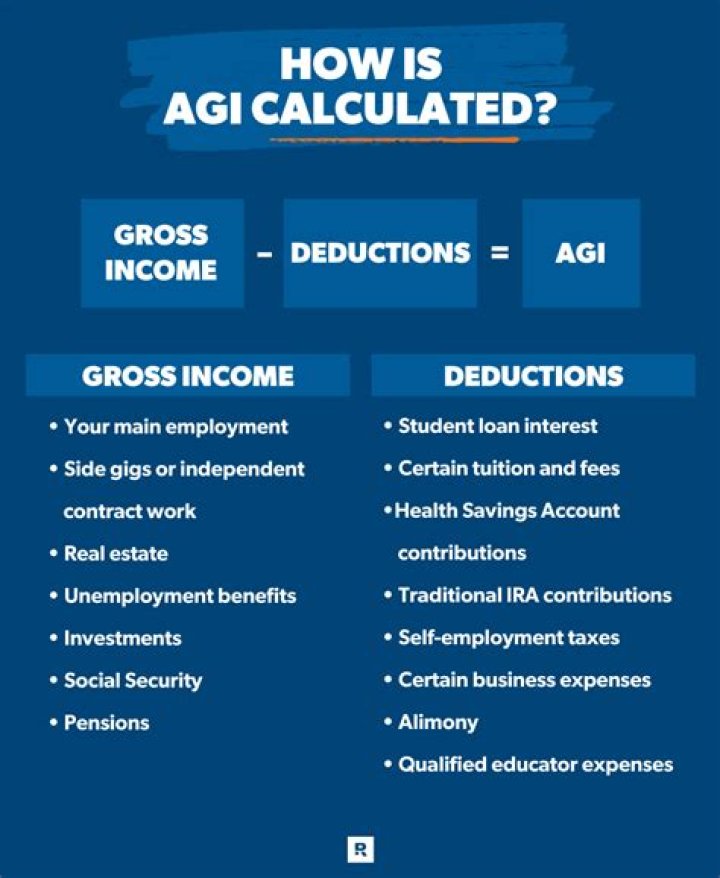

- Start with your gross income. Income is on lines 7-22 of Form 1040.

- Add these together to arrive at your total income.

- Subtract your adjustments from your total income (also called “above-the-line deductions”)

- You have your AGI.

What if my standard deduction is more than my adjusted gross income?

If your deductions exceed income earned and you had tax withheld from your paycheck, you might be entitled to a refund. You may also be able to claim a net operating loss (NOLs). A Net Operating Loss is when your deductions for the year are greater than your income in that same year.

It includes wages, interest, dividends, business income, rental income, and all other types of income. Adjusted gross income is gross income less deductions from a business or rental activity and 21 other specific items.

Does 529 reduce AGI?

Contributing to an education plan like qualified tuition programs (QTPs, or 529 plans) and Coverdell Education Savings Accounts (ESAs) will not qualify you for a deduction on your federal return.

Why is adjusted gross income important to the IRS?

Adjusted gross income (AGI) is your gross income — i.e., the total amount of money you’re paid before taxes are taken out—minus certain deductions allowed by the IRS. Adjusted gross income is important because for many Americans it serves as the starting point for determining how much they’ll have to pay in taxes each year.

How is the Adjusted Gross Income ( SOI ) calculated?

The Statistics of Income (SOI) Division’s adjusted gross income (AGI) percentile data by State are based on individual income tax returns (Forms 1040) filed with the Internal Revenue Service (IRS) during a given tax year.

What is the adjusted gross income for 2019?

If your 2019 tax return has not yet been processed, enter $0 (zero dollars) for your prior year adjusted gross income (AGI). If you used the Non-Filers: Enter Payment Info Here tool in 2020 to register for an Economic Impact Payment in 2020, enter $1 as your prior year AGI.

How often does your accountant mention adjusted gross income?

Perhaps your accountant mentions it in passing whenever you get your taxes done, or you recognize it as a line item on your annual tax returns. But without context, it’s hard to understand just how important it is.