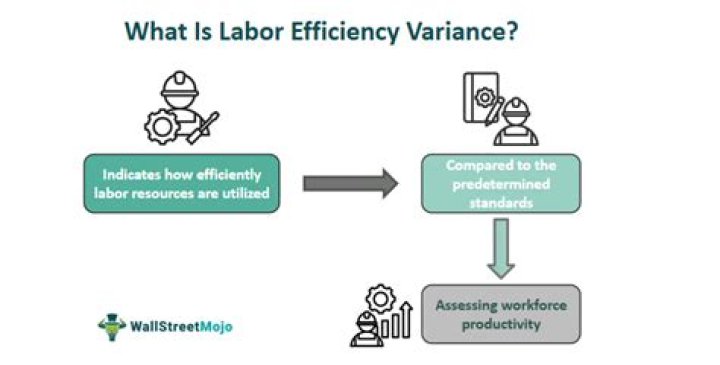

What causes unfavorable labor efficiency variance?

Henry Morales

Published Feb 18, 2026

Variance is unfavorable because the actual hours of 97,500 are higher than the expected (budgeted) hours of 78,000. A higher mix of newly hired and unskilled workers caused hourly rates to be lower than anticipated; A new labor contract was negotiated at lower pay rates than anticipated.

Why is cost variance?

Cost variance is the process of evaluating the financial performance of your project. Cost variance compares your budget that was set before the project started and what was spent. This is calculated by finding the difference between BCWP (Budgeted Cost of Work Performed) and ACWP (Actual Cost of Work Performed).

How do you prevent adverse variance?

For example, if your budgeted expenses were $200,000 but your actual costs were $250,000, your unfavorable variance would be $50,000 or 25 percent. Often budget variances can be eliminated by analyzing your expenses and allocating an expensed item to another budget line.

How do you handle budget variances?

Cutting expenses, avoiding new expenditures and reallocating assets or manpower are some methods to closing the variance. Continue to compare the budget to actual numbers until the budget variance is minimal.

How do you interpret cost variance?

Cost Variance indicates how much over or under budget the project is in terms of percentage.

- Positive = indicates how much under budget the project.

- Negative = indicates how much over budget the project.

How do you reduce variance?

The principles used to reduce the variance for a population statistic can also be used to reduce the variance of a final model. We must add bias….Reduce Variance of a Final Model

- Ensemble Predictions from Final Models.

- Ensemble Parameters from Final Models.

- Increase Training Dataset Size.

When should you start investigating a variance?

When should a variance be investigated – factors to consider

- Size. A standard is an average expected cost and therefore small variations between the actual and the standard are bound to occur.

- Favourable or adverse.

- Cost.

- Past pattern.

- The budget.

- Reliability of figures.