What are the similarities and differences between depreciation depletion and amortization?

Mia Ramsey

Published Feb 17, 2026

Depreciation spreads out the cost of a tangible asset over its useful life, depletion allocates the cost of extracting natural resources, such as timber, minerals, and oil from the earth, and amortization is the deduction of intangible assets over a specified time period; typically the life of an asset.

What is the difference between accumulated depreciation and depreciation?

Accumulated depreciation is the total amount a company depreciates its assets, while depreciation expense is the amount a company’s assets are depreciated for a single period.

What are the similarities and differences between the terms depreciation depletion and amortization quizlet?

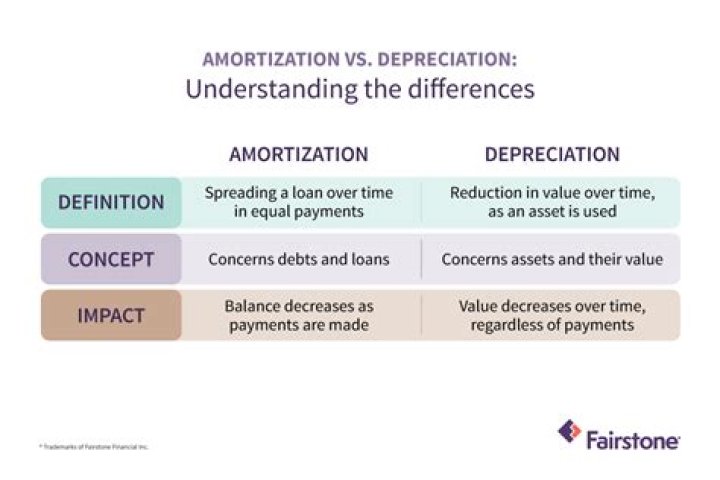

The only difference between the terms is that they refer to different types of these long-lived assets; depreciation for plant and equipment, depletion for natural resources, and amortization for intangibles. Depreciation is a process of cost allocation, not valuation.

What does it mean when depreciation and amortization increases?

You increase it with a credit because it essentially is a substitute for reducing the cost of an asset as it loses value over time. For example, when Smalltown has a fully depreciated van, the net asset value would be zero – the cost of the asset minus the value of its accumulated depreciation.

Why does depreciation and amortization increase?

Operating cash flow starts with net income, then adds depreciation/amortization, net change in operating working capital, and other operating cash flow adjustments. The result is a higher amount of cash on the cash flow statement because depreciation is added back into the operating cash flow.

What is the objective of accounting for depreciation?

The purpose of depreciation is to achieve the matching principle of accounting. That is, a company is attempting to match the historical cost of a productive asset (that has a useful life of more than a year) to the revenues earned from using the asset.

What is meant by depreciable base How is it determined?

Definition. The financial accounting term depreciable base is used to describe the value that is divided by the service life of the asset to determine the annual depreciation expense under the straight line method. The depreciable base is the value of the asset to be written off over time.

Why do we use depreciation?

Assets such as machinery and equipment are expensive. Instead of realizing the entire cost of the asset in year one, depreciating the asset allows companies to spread out that cost and generate revenue from it. Depreciation is used to account for declines in the carrying value over time.