What are the key differences between cash and accrual accounting?

Emma Jordan

Published Feb 19, 2026

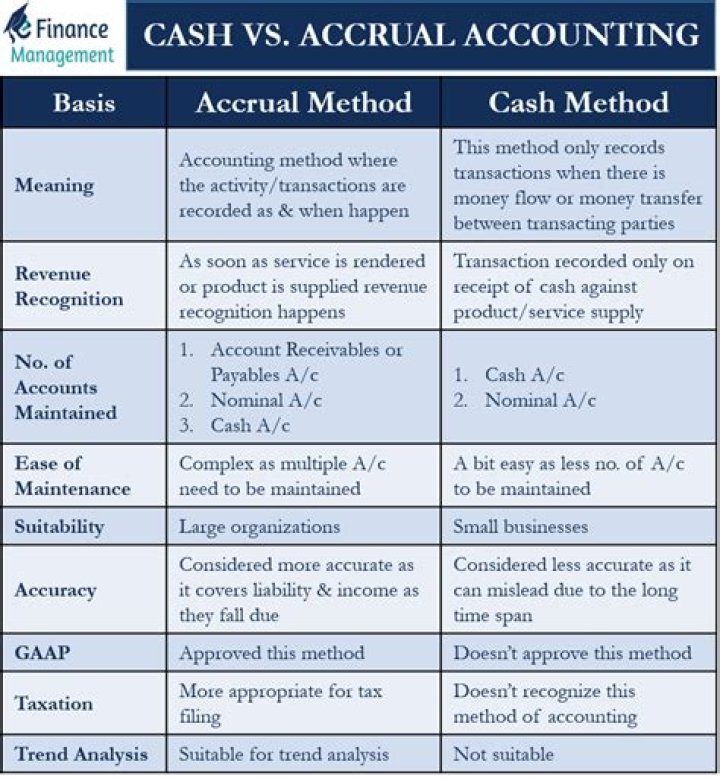

The difference between cash and accrual accounting lies in the timing of when sales and purchases are recorded in your accounts. Cash accounting recognizes revenue and expenses only when money changes hands, but accrual accounting recognizes revenue when it’s earned, and expenses when they’re billed (but not paid).

What determines whether a transaction shows up on a cash or accrual report?

What’s the Difference Between Cash and Accrual Accounting? Your accounting method determines when transactions should be reported on your financial statements. In the accrual method, you report your accrued income and expenses when they were earned or incurred regardless of when the cash changes hands.

What do you think are the benefits of using accrual accounting over the cash method of accounting?

While cash-based accounting can give a point-in-time picture of the business cash flow, accrual-based accounting offers a more accurate picture of the longer-term state of the business; revenues and expenses are immediately recorded, allowing the business to more properly analyze trends and manage finances.

How do you determine cash or accrual?

The cash basis method generally recognizes income when cash is received and expenses when cash is paid. The accrual method recognizes income when it is earned (the creation of assets such as accounts receivable) and expenses when they are incurred (the creation of liabilities such as accounts payable).

Can I switch between cash and accrual?

If you want to change from using the accrual accounting method to cash basis accounting, you will ordinarily need to request permission to do so by filing Form 3115 with the IRS.

How do you convert cash to accrual?

To convert to accrual, subtract cash payments that pertain to the last accounting period. By moving these cash payments to the previous period, you reduce the current period’s beginning retained earnings. Cash receipts received during the current period might need to be subtracted.

What is the difference between cash method and accrual method?

The main difference between accrual and cash basis accounting lies in the timing of when revenue and expenses are recognized. The cash method is a more immediate recognition of revenue and expenses, while the accrual method focuses on anticipated revenue and expenses.

Does accrual basis of accounting recognize expenses when cash is paid?

The accrual basis of accounting recognizes revenues when earned (a product is sold or a service has been performed), regardless of when cash is received. Expenses are recognized as incurred, whether or not cash has been paid out.

What is the difference between accrual accounting and cash?

The accrual method is essentially a matching up of revenues to expenses when the transaction takes place instead of when payment is processed or received, which is the cash basis accounting method.

What are the drawbacks of accrual accounting?

Besides this, one of the major drawbacks of accrual accounting is that the company has to pay tax on the income which is not yet received. The accounting system in which the income or expense is recognised when an exchange of consideration is actually done is known as Cash Accounting.

When to recognize revenue on a cash or accrual basis?

Revenue recognition. A company sells $10,000 of green widgets to a customer in March, which pays the invoice in April. Under the cash basis, the seller recognizes the sale in April, when the cash is received. Under the accrual basis, the seller recognizes the sale in March, when it issues the invoice. Expense recognition.

When to use accrual accounting for tax purposes?

Accrual Accounting. Accrual accounting is the most common accounting practice for corporations. Businesses with annual revenues in excess of $5 million are required to use the accrual method for tax purposes. The impetus for using the accrual method of accounting comes from increasingly complex business transactions,…