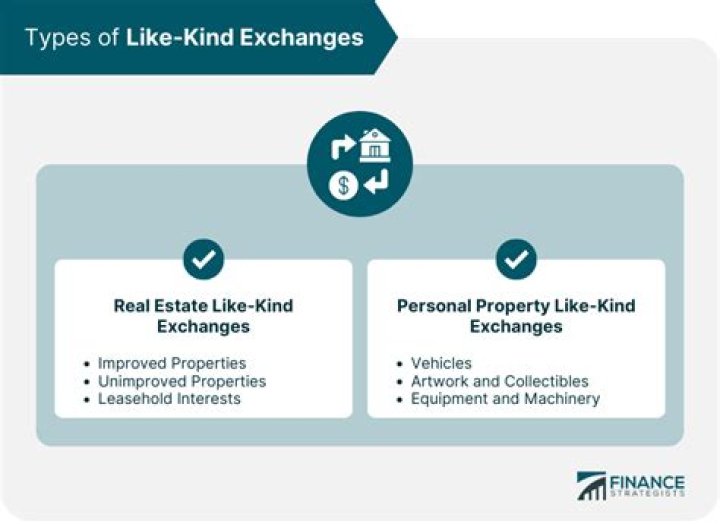

What are examples of like-kind exchanges?

Andrew Mclaughlin

Published Feb 27, 2026

The IRS considers all “Investment Properties” to be “Like-Kind.” Properties do not need to be the same type. For example, raw land can be exchanged for an office building, a warehouse can be exchanged for NNN retail property, or a rental house for a Replacement Property Interest in a 300-unit apartment complex.

How do you record a deferred gain?

As a liability, the recorded deferred gains are listed on the right side of the balance sheet equation in liabilities. Understanding how the balance sheet works help clarify why gains are considered a liability until they are realized as an asset, thus gain.

Why is deferred gain a liability?

When a company accrues deferred revenue, it is because a buyer or customer paid in advance for a good or service that is to be delivered at some future date. The payment is considered a liability because there is still the possibility that the good or service may not be delivered, or the buyer might cancel the order.

What do you need to know about 1031 like kind exchange?

If you’ve recent ly completed a 1031 like-kind exchange, you need to document your transaction for your accounting records.Although a deferred gain is an unearned revenue, it represents a future asset that counts as a liability on your balance sheet. Gains are seen as a liability until realized as an asset.

What are the accounting rules for like kind exchanges?

Internal Revenue Code Sec. 1031 governs the tax accounting treatment of like-kind exchanges. Sec. 1031(a)(1) requires that both the asset given up and the asset received must be held for investment or for productive use in a trade or business. The properties must also be of like kind.

When does a like-kind exchange take place?

When a like-kind exchange takes place the gain or loss realized on the exchange must be determined. The gain or loss that is recognized depends upon whether a gain or loss was realized and whether any boot was received. The financial accounting and tax accounting treatment given to like-kind exchanges often differs.

What happens if you do not report a 1031 exchange?

Failure to report your exchange can result in ineligibility for capital gains tax deferral and other costly penalties. A deferred gain in a 1031 exchange is the amount of gain that evades taxation until the acquired property from the exchange is sold for profit. Let’s examine this from an accounting perspective.