What are cheapest to deliver bonds?

James Craig

Published Feb 18, 2026

What Is Cheapest to Deliver?

- Cheapest to deliver is the cheapest security that can be delivered in a futures contract to a long position to satisfy the contract specifications.

- It is common in Treasury bond futures contracts.

What factor provided by the futures exchange would be needed to calculate the invoice amount for the cheapest to deliver government bond?

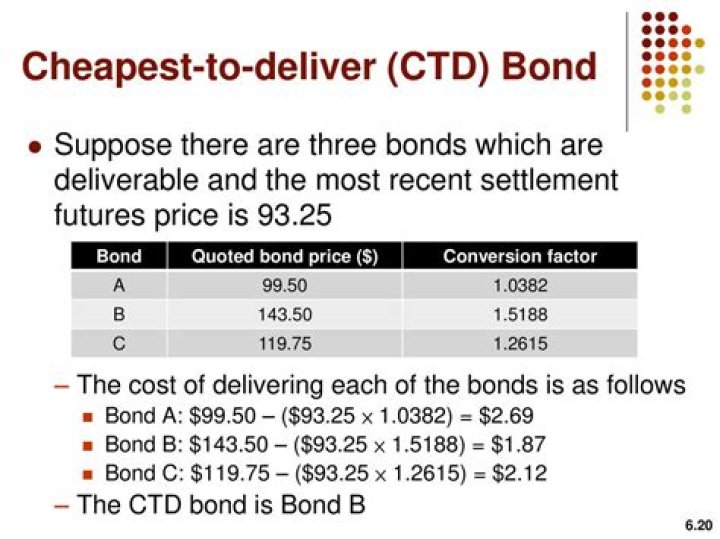

The conversion factor (CF) for the cheapest to deliver bond (CTD) is an important concept used to price fixed income futures. The conversion factor is needed to determine the principal invoice price. This is the price that the short party of a fixed income futures will receive upon settlement.

What is a bond conversion factor?

The conversion factor, for any particular bond deliverable into a futures contract, is a number by which the bond futures delivery settlement price is multiplied, to arrive at the delivery price for that bond.

Can you do a 10 year bond future?

The 10-year Treasury note futures, or 10-year T-note futures, are a debt obligation issued by the U.S. government that matures in 10 years. A 10-year Treasury note futures contract pays interest at a fixed rate once every six months and pays the face value to the holder at maturity.

What is contribution to duration?

Spread duration contribution equals the spread duration of a security or market segment multiplied by the size of the allocation to it.

What does Bond duration tell you?

Bond duration is a way of measuring how much bond prices are likely to change if and when interest rates move. In more technical terms, bond duration is measurement of interest rate risk. Understanding bond duration can help investors determine how bonds fit in to a broader investment portfolio.

What is the current Treasury bond rate?

Treasury Yields

| Name | Coupon | Yield |

|---|---|---|

| GT2:GOV 2 Year | 0.13 | 0.20% |

| GT5:GOV 5 Year | 0.88 | 0.77% |

| GT10:GOV 10 Year | 1.63 | 1.33% |

| GT30:GOV 30 Year | 2.38 | 1.97% |

What is the difference between duration and spread duration?

Spread duration should not be confused with duration, which is an estimate of a bond’s price sensitivity to interest rates. Spread duration is a bond’s price sensitivity to spread changes. Spread duration is an estimate of how much the price of a specific bond will move when the spread of that specific bond changes.

What are the limits of duration as a risk measure?

The main limitation of duration is that it assumes a linear relationship between interest rates and bond price. In reality, the relationship is likely to be curvilinear. The extent of the deviation from a linear relationship is known as convexity.

What is duration formula?

What is the Duration Formula? The formula for the duration is a measure of a bond’s sensitivity to changes in the interest rate, and it is calculated by dividing the sum product of discounted future cash inflow of the bond and a corresponding number of years by a sum of the discounted future cash inflow.