What amount of the contribution is deductible?

Henry Morales

Published Feb 12, 2026

Individuals may deduct qualified contributions of up to 100 percent of their adjusted gross income. A corporation may deduct qualified contributions of up to 25 percent of its taxable income. Contributions that exceed that amount can carry over to the next tax year.

Can I claim my contribution as a deduction on my tax return?

If your income is under the limits, you’re eligible to claim a tax deduction for your contributions to a traditional IRA. If you’re in the income phase-out range, you can deduct a portion of your contributions. If your income is higher than the maximum income limit, then you can’t deduct your IRA contributions.

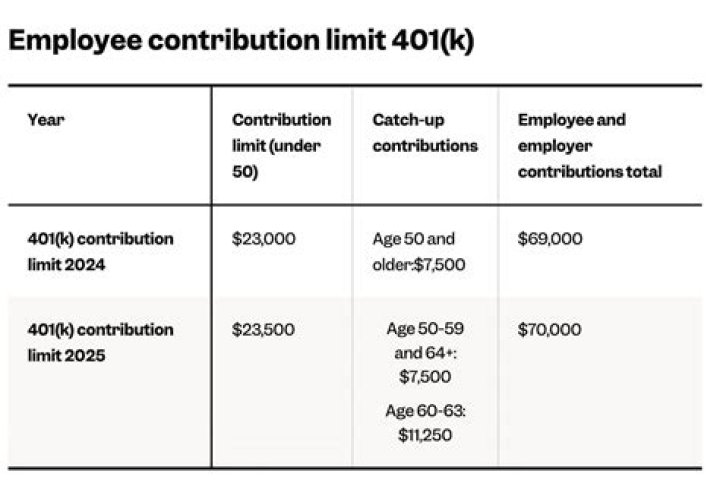

How much 401k contribution is tax deductible?

When planning for retirement, investors might hear about a “401(k) tax deduction.” But while there are tax benefits associated with contributing to a 401(k) account, there is no such thing as a 401(k) tax deduction. Any money contributed to a 401(k) is not included in the employee’s taxable income for that year.

What does it mean when contributions are tax deductible?

Tax deductible donations are contributions of money or goods to a tax-exempt organization such as a charity. Tax deductible donations can reduce taxable income. To claim tax deductible donations on your taxes, you must itemize on your tax return by filing Schedule A of IRS Form 1040 or 1040-SR.

Are Solo 401k contributions tax-deductible?

In a Solo 401(k) plan all contributions you make as the “employer” will be tax-deductible (subject to IRS maximums) to your business with any earnings growing tax-deferred until withdrawn. But for contributions you make as an “employee” you have more flexibility.

What are the IRA contribution limits for 2017?

It’s important to note that these are per-person limits, not per account. In other words, if you’re under 50 and have more than one IRA, your total contribution to all of your IRA accounts cannot exceed $5,500 for 2017. You can make your IRA contribution for 2017 as a lump sum, or you can contribute a little at a time.

What are the tax deductions for charitable contributions?

A corporation may deduct qualified contributions of up to 25 percent of its taxable income. Contributions that exceed that amount can carry over to the next tax year. To qualify, the contribution must be: a cash contribution; made to a qualifying organization; made during the calendar year 2020

What are the tax deductions for pension contributions in South Africa?

Contributions to a pension, provident or retirement annuity fund during a tax year are deductible by the member of the fund. The deduction is limited to the greater of: 27.5% of the employee’s taxable income (excluding retirement fund lump sums and severance benefits). The deduction is limited to a maximum amount of R 350 000.

Can you deduct qualified contributions on your taxes?

Qualified contributions are not subject to this limitation. Individuals may deduct qualified contributions of up to 100 percent of their adjusted gross income. A corporation may deduct qualified contributions of up to 25 percent of its taxable income. Contributions that exceed that amount can carry over to the next tax year.