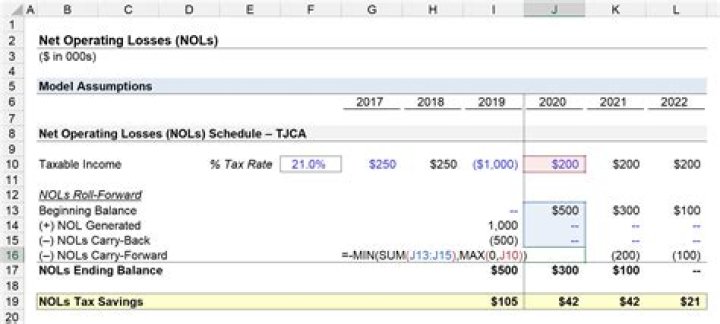

What amount of NOL can be carried forward to 2020?

Ava Robinson

Published Mar 31, 2026

The TCJA eliminated NOL carrybacks and permitted NOLs to be carried forward indefinitely. The CARES Act changes those rules temporarily by permitting NOLs incurred in 2018, 2019, or 2020 to be carried back for five years to the earliest year first and suspending the 80% taxable income limitation through 2020.

Can a taxpayer carryback an NOL to specific years?

A taxpayer must make an election either to exclude section 965 years from the carryback period for an NOL arising in a taxable year beginning in 2018 or 2019, or to waive the carryback period for such an NOL by the due date (including extensions) for filing its return for the first taxable year ending after March 27.

Can you skip years in an NOL carryforward?

If your NOL amount is more than your taxable income during the five-year carryback period, you can carry any remaining NOL amount forward. You have to apply the NOL to the fifth preceding year first then work your way forward to a more recent tax year.

What happens to NOL credits in the carryover year?

Carrybacks from an unused credit year are applied against tax liability before carrybacks from a later unused credit year. To the extent an unused credit cannot be carried back to a particular preceding taxable year, the unused credit must be carried to the next succeeding taxable year to which it may be carried.

Can you carryback NOL in 2020?

Unless an election is made to forego the entire carryback, an NOL arising in a taxable year beginning in 2018, 2019 or 2020 must be carried back to the earliest year within the carryback period in which there is taxable income, then to the next earliest year, and so on.

What is NOL carryover on tax returns?

A Net Operating Loss (NOL) Carryforward allows businesses suffering losses in one year to deduct them from future years’ profits. Businesses thus are taxed on average profitability, making the tax code more neutral.

How is a NOL / tax loss carryforward can lower?

What is an NOL / Tax Loss Carryforward? A Net Operating Loss (NOL) or Tax Loss Carryforward is a tax provision that allows firms to carry forward losses from prior years to offset future profits, and therefore, lower future income taxes Accounting For Income TaxesIncome taxes and its accounting is a key area of corporate finance.

How to calculate Nol carryover for 2020 tax return?

You can use Form 1045, Schedule B, to figure your modified taxable income for carryback years and your carryover from each of those years. If your 2020 return includes an NOL deduction from an NOL year before 2018 that reduced your taxable income to zero (to less than zero, if an estate or trust), see NOL Carryover From 2020 to 2021 below.

What are the new rules for net operating loss carryover?

The Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) has relaxed the rules for the carryover of Federal net operating losses (“NOLs”). The 2017 Tax Cuts and Jobs Act (“TCJA”) eliminated the 2-year carryback rule for any operating losses arising in tax years ending after December 31, 2017.

When does the NOL carryover period end for 2017?

In addition, the deduction of the NOLs arising in taxable years beginning after December 31, 2017 was limited to 80% of taxable income under the TCJA. The CARES Act gives businesses a five-year carryback period of NOLS arising in a taxable year beginning after December 31, 2017 and before January 31, 2021.