Is there a limit to UTMA contributions?

Henry Morales

Published Feb 22, 2026

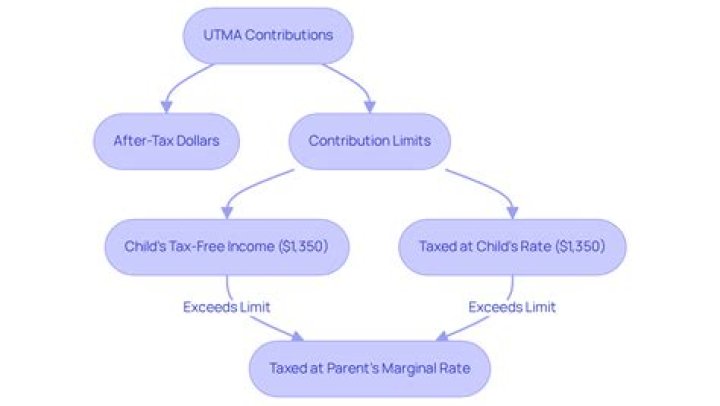

Who should consider a UGMA/UTMA account? Anyone can contribute up to $15,000 per child each year free of gift-tax consequences ($30,000 for married couples). This amount is indexed for inflation and may increase over time. Because contributions are made with after-tax dollars, a deduction cannot be taken.

Are contributions to UTMA accounts tax deductible?

UGMA/UTMA Contributions Contributions are not tax-deductible, however, you can give up to $15,000 (2020 and 2021) per year ($30,000 for a married filing jointly couple) without incurring federal gift tax. Contributions are irrevocable as well. Meaning, once you transfer to the minor’s account, you can’t get it back.

What’s the income limit for a UTMA account?

For 2019, the limit for unearned income for minors is $2,200. Amounts above that are taxed at the rate applicable to trusts and estates. These tax rates vary depending on the amount. Regardless, there is very little tax advantage to establishing UTMA accounts.

What’s the difference between tax free UGMA and UTMA?

In 2021, the first $1,100 in a UGMA or UTMA is considered tax-free, and the next $1,100 is taxed at the child’s bracket, which is 10% for federal income tax. 2 3 4 Anything above those amounts is taxed at the parents’ rate, which may be as high as 37%. This exemption is per child, not per account.

How old do you have to be to transfer UTMA funds?

Unused Funds. For classic UGMA accounts, this generally occurs at the age of 18. For the newer UTMA accounts, this age is usually 21—but may be as late as age 25. Unlike Section 529 plans and Coverdell ESA’s, there’s no ability to transfer the account to another child or change beneficiaries.

Who is the custodian of UGMA and UTMA accounts?

UGMA and UTMA Custodial Accounts allow adults to make financial gifts to a beneficiary while naming someone else (including themselves) as the custodian of the account. The crucial word for these accounts is “gift.”