Is the mortgage interest deduction grandfathered?

James Craig

Published Feb 21, 2026

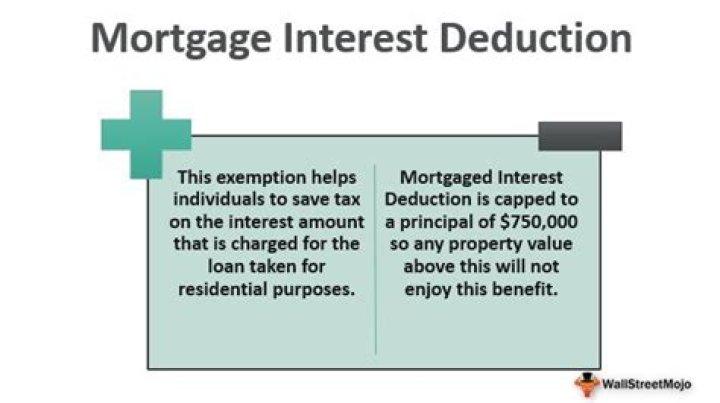

Under TCJA, mortgage interest is deductible if the home acquisition debt is $750,000 or less ($375,000 for married filing separate) on one or two homes for 2018 through 2025. Debt incurred on or before December 15, 2017 is grandfathered in under the old rules for home acquisition debt of $1 million or less.

Can you deduct mortgage interest 2017?

You can deduct home mortgage interest on the first $750,000 ($375,000 if married filing separately) of indebtedness. However, higher limitations ($1 million ($500,000 if married filing separately)) apply if you are deducting mortgage interest from indebtedness incurred before December 16, 2017.

Why did my mortgage payment go up after a year?

You have an escrow account to pay for property taxes or homeowners insurance premiums, and your property taxes or homeowners insurance premiums went up. If your monthly mortgage payment includes the amount you have to pay into your escrow account, then your payment will also go up if your taxes or premiums go up.

Can a bank raise your mortgage?

Mortgage Payments Can Increase with Interest Rate Adjustments. Here’s the easy one. If you happen to have an adjustable-rate mortgage, your mortgage rate has the ability to adjust both up or down, as determined by the interest rate caps.

What’s the limit for taking out a mortgage after 2017?

For mortgages taken out after 2017, the combined total of mortgage debt plus additional home equity debt (used to improve or renovate a house) is capped at the new $750,000 threshold. Are you thinking of purchasing a second home??

What was the mortgage interest deduction in 2017?

That’s down from the 32.3 million filers who got the deduction on their 2017 taxes. To put it another way, the savings from mortgage interest deduction are expected to drop to $25.01 billion on 2018 returns — down from $59.87 billion last year. Why such a stark change coming?

What should I get when my mortgage is paid off?

Even better, if you have a final statement from the lender, it should show that your loan was paid in full. Most title companies can use those documents as evidence that a loan from almost 20 years ago was paid off.

Is the mortgage interest deduction going away for 2018?

With the mortgage interest deduction going away for an estimated 18 million taxpayers, it’s safe to say there’s no time like the present to pay off your mortgage — if doing so is within your means.