Is tax basis inside or outside?

Andrew Mclaughlin

Published Mar 01, 2026

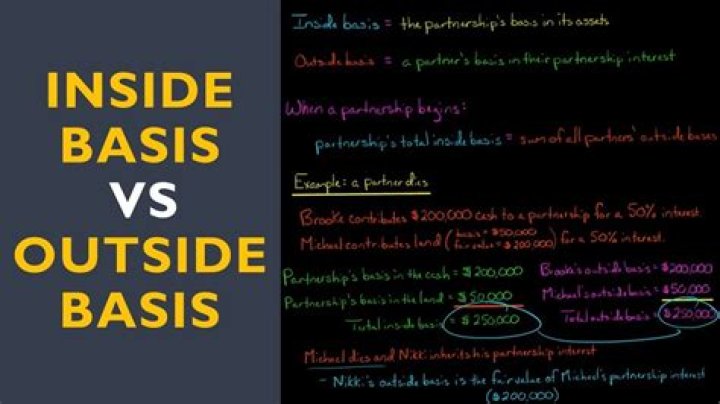

Partnership tax law often refers to “outside” and “inside” basis. Outside basis refers to a partner’s interest in a partnership. Inside basis refers to a partnership’s basis in its assets.

What is inside basis vs outside basis?

The inside basis is the partnership’s tax basis in the individual assets. The outside basis is the tax basis of each individual partner’s interest in the partnership. When a partner contributes property to the partnership, the partnership’s basis in the contributed property = its fair market value ( FMV ).

How do you calculate outside basis?

A tax investor’s tax or outside basis is equal to the total of :

- the capital contribution by the investor (initial capital contribution or amount paid by the tax investor),

- additional capital contributions (not generally there),

- dividends paid from the pre-tax cash flow distributions (that are subtracted)

Does tax exempt income increase outside basis?

Common items that increase a partner’s outside basis are: The increased share of partnership liabilities in the year. Any recognition of income, including tax exempt income.

How does tax exempt income affect basis?

After basis has been reduced by distributions is it then reduced by nondeductible expenses – for the same reason basis is increased by tax-exempt income: to preserve the nondeductible nature of the expenses – and only THEN reduced by non-separately stated and separately stated losses.

What is the basis for tax purposes?

Basis is generally the amount of your capital investment in property for tax purposes. Use your basis to figure depreciation, amortization, depletion, casualty losses, and any gain or loss on the sale, exchange, or other disposition of the property. In most situations, the basis of an asset is its cost to you.

What’s the difference between inside basis and outside basis?

Inside Basis vs Outside Basis – Outside Basis Outside basis represents each partner’s basis in the partnership interest. Each partner “owns” a share of the partnership’s inside basis for all of its assets, and all partners should maintain a record of their respective outside bases.

How is the outside basis determined in a partnership?

This determines the partner’s tax basis according to the respective individual assets contributed to the operation of the business. Outside basis represents each partner’s basis in the partnership interest.

Where does 743 ( B ) go on a partner’s tax basis?

However, the draft instructions note that Section 743(b) adjustments are not included in a partner’s tax basis capital account and, if included in a partner’s beginning capital account balance, should be removed from the partner’s capital account in the 2020 tax year and reported as an “other increase (decrease) item.”

How does the modified outside basis method work?

The modified outside basis method requires the partnership to either determine the outside basis of the partners or be provided the outside basis by its partners.