Is it worth opening a 529 plan?

Andrew Ramirez

Published Apr 09, 2026

Known as a qualified tuition plan, a 529 plan allows you to save money for your child’s college education that grows tax-free. While plans differ from state to state, the opportunity to let your money compound tax-free is certainly attractive.

How much do you need to start 529?

If all you can afford when you open your 529 plan is an initial contribution of $50 or $100, that’s fine; you can plan to build your account over time, contributing as much as you can afford. Many families start their 529 plan with small deposits at first, and every dollar added is less debt down the road.

Many people saving for college choose 529 plans as their investment vehicles, and that’s for good reason. 529 plans offer tax advantages that can help you allocate even more dollars to education expenses. There are a variety of plans available, and you’re not limited to just your own state’s plan.

What documentation do I need for 529?

Form 1099-Q

In each year you take withdrawals from a 529, the plan administrator should issue a Form 1099-Q, which reports the total distribution taken from the account in a given year, the portion of the distribution that came from earnings in the account, and the portion of the distribution that represents the original …

Are 529 bogleheads worth it?

The 529 is definitely worth it if you are absolutely sure the money will be spent on qualified expenses and you max out all retirement accounts/HSA. Actually, you are in what I would call an ideal situation for one given that you have 3 kids and a long time horizon.

Who Should 529 distributions attend?

How to report a taxable 529 plan distribution on federal income tax returns. The earnings portion of a taxable 529 plan distribution must be reported on the beneficiary’s or the 529 plan account owner’s tax returns.

What should you have in a 529 plan?

So let’s dive in and see how much you should have in a 529 plan. As a parent, you should also have solid term life insurance to protect your family. Beyond saving for college, this is a must for taking care of your children.

Who is the owner of a 529 savings plan?

Anyone can open and fund a 529 savings plan—the student, parents, grandparents, or other friends and relatives. Unlike a custodial account that eventually transfers ownership to the child, with a 529 savings plan, the account owner (not the child) calls the shots on how and when to spend the money.

Can a cell phone be expensed in a 529 plan?

General Electronics and Cell Phone Plans – Cell phones are an everyday part of life. As such, they are not considered an education expense, and while “necessary”, they can’t be expensed and paid for with your qualified distributions from your 529 plan.

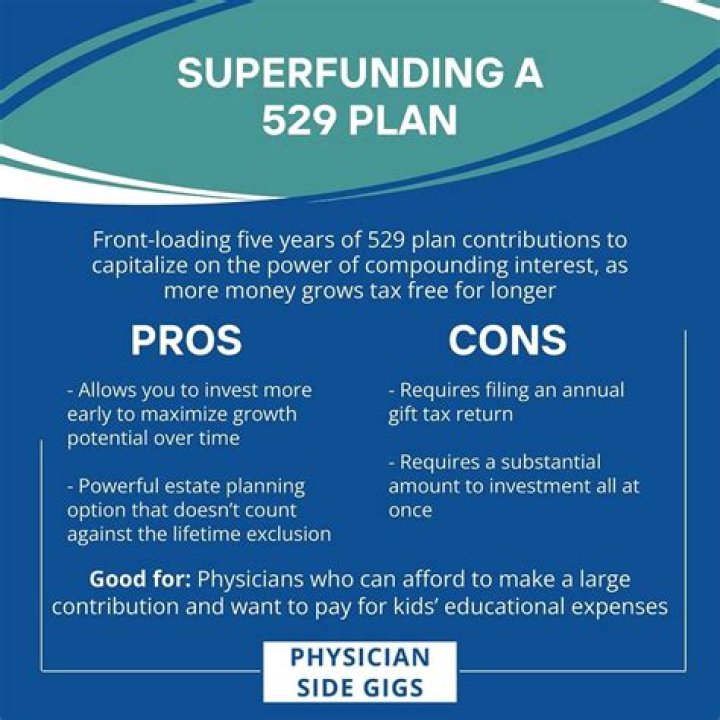

Why do you need to front load your 529 plan?

Why You Should Front-Load Your 529 Plan. The purpose of a 529 plan is to pay future education costs, typically for a child or grandchild. Before passage of the Tax Cuts and Jobs Act of 2017 (TCJA), 529s could be used only for college costs. Now they can be used for private K-12 education costs as well.