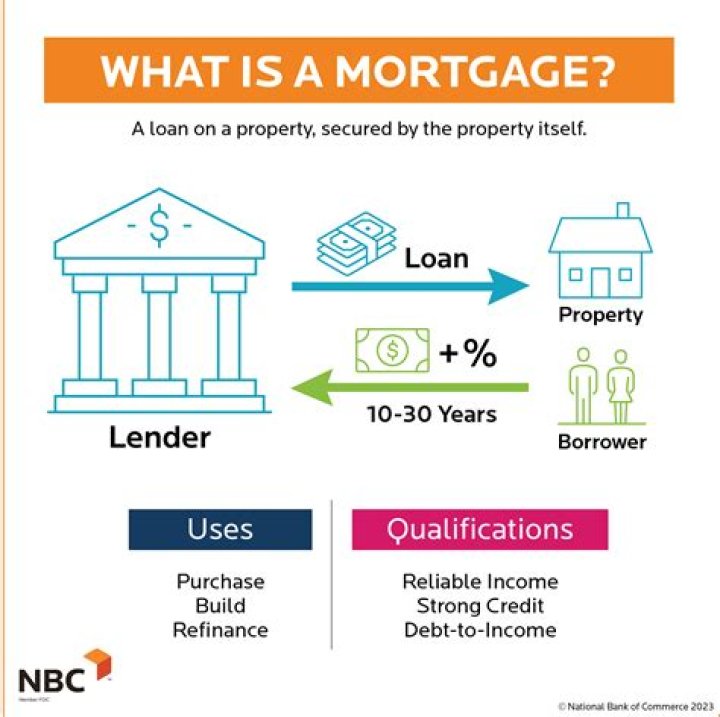

Is home mortgage a debt?

James Williams

Published Feb 24, 2026

A home mortgage is one of the most common forms of debt, and it is also one of the most recommended. Because they are secured debt—there is an asset (the residence) acts as backing for the loan—mortgages come with lower interest rates than almost any other kind of loan an individual consumer can find.

How much debt is acceptable for a mortgage?

Most lenders will lend below 100% debt-to-income ratio. 50% is a common limit, but some lenders are more cautious. At the time of writing, only one lender does not lend to applicants with a debt-to-income ratio above 25%.

Can you get a mortgage with outstanding debt?

In a word, yes. Regardless of the myth that arrears of any kind will ruin your chances, you may still be able to get a mortgage whilst having an outstanding debt. When applying for a mortgage, you’ll need to come across as attractive as possible to lenders.

What kind of debt is a home mortgage?

Most consider home mortgage for one’s primary residence under the category of an obligation against future income or wealth. That is, strictly speaking, a home mortgage, though a debt, applies in actuality and agreement to the income one will earn in the future.

Can a medical student get a high debt mortgage?

For instance, some lenders offer high-DTI loans for graduating medical students, because their income increases substantially once they start work. If you know you’ll be getting a significant sum in the next few months or years, a high debt mortgage could get you into a home faster.

Can you get a mortgage if you have a lot of debt?

Mortgage with debt When underwriting your mortgage application, lenders don’t just consider your income. They look at the relationship between what you earn and what you spend — your debt-to-income ratio, or DTI. If your DTI is on the high side, getting a mortgage could be a challenge.

When to buy a home with high debt?

If you know you’ll be getting a significant sum in the next few months or years, a high debt mortgage could get you into a home faster. And you’ll be able to afford it soon enough. This may also be true if you have big expenses going away — for example, your child will graduate from college and those tuition costs will vanish.