Is 1250 property subject to recapture?

Andrew Mclaughlin

Published Apr 04, 2026

Gain from selling Sec 1250 property (real estate) is subject to recapture – the excess of the actual amount of depreciation previously claimed for the property over the amount of depreciation that would have been allowable under the straight-line method, limited to the gain on the sale, is taxed as ordinary income.

What assets are subject to 1250 recapture?

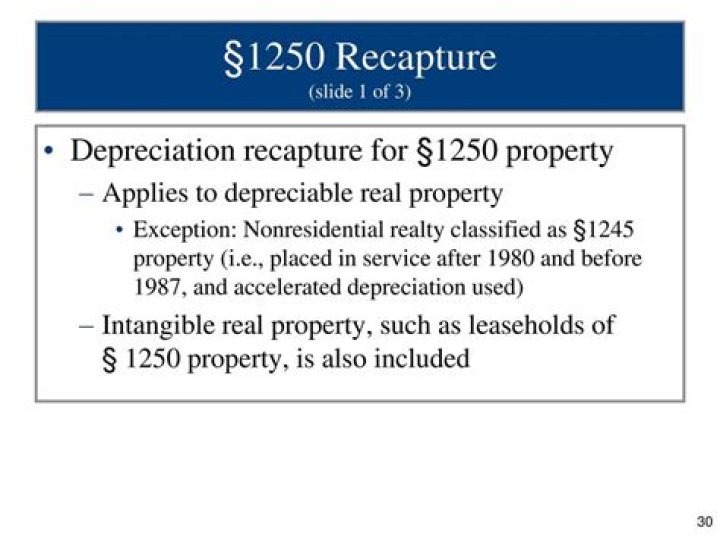

Unrecaptured Section 1250 gain only applies to depreciable real estate, such as commercial real estate and residential rental properties. For example, if an investor purchases an income property for $200,000 and has claimed $50,000 for depreciation deductions, the adjusted cost basis is now $150,000.

What property is subject to depreciation recapture?

A capital gains tax applies to depreciation recapture that involves real estate and properties. The depreciation recapture for equipment and other assets, however, doesn’t include capital gains tax.

Is Section 1250 a property?

Section 1250 addresses the taxing of gains from the sale of depreciable real property, such as commercial buildings, warehouses, barns, rental properties, and their structural components at an ordinary tax rate. However, tangible and intangible personal properties and land acreage do not fall under this tax regulation.

What is the recapture rule for 1250 real estate?

Since your gain is greater than your accumulated tax depreciation, the recapture rule will apply. As a result, your tax on sale is not $9,750 ($65,000 x 15%), but rather $12,250, 25.6% more in taxes than what you planned! The amount subject to the higher (25% or ordinary) rates is limited to the gain on the Sec. 1250 property.

When does Section 1245 apply to depreciation recapture?

Sections 1245 and 1250 generally apply to any transfer of depreciable property (including certain property that is expensed under rules similar to depreciation rules, such as rapid amortization property and property that has been expensed under §179). Certain transfers of depreciable property, however, are excepted from depreciation recapture.

Are there limits to the recapture of depreciation?

1 In 2019, depreciation recapture on gains related to the sale of the property was capped at a maximum of 25%. 2 In the U.S., depreciation recapture is governed by sections 1245 and 1250, according to the Internal Revenue Code (IRC). 3 There is no depreciation recapture if a taxpayer sells an asset for a loss.

How are recapture and Unrecaptured real estate gains taxed?

Recaptured and Unrecaptured Real Estate Rental Section 1250 Gain. But the amount of depreciation claimed on Sec 1250 property that is not recaptured as ordinary income under the Sec1250 recapture rules is unrecaptured section 1250 gain, and is subject to a special capital gain tax rate of 25%.