Is 1120h required?

Emma Jordan

Published Apr 11, 2026

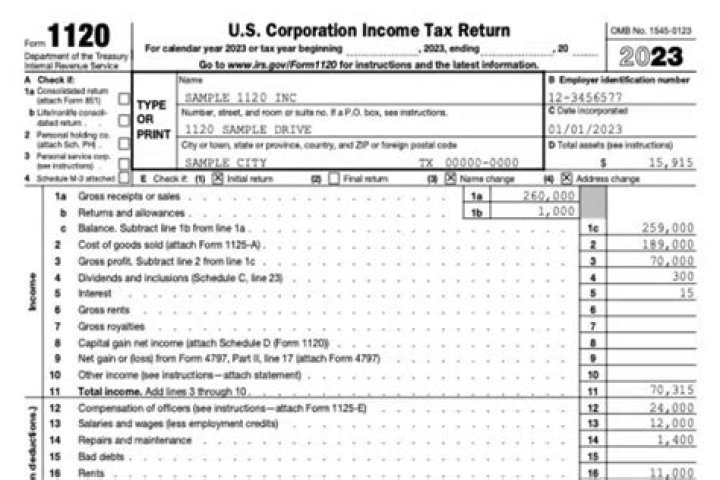

Initially, HOAs had to file Form 1120, which is the corporate income tax return. Form 1120 is more complicated and does not exempt the payment of tax on dues and assessments. However, after the Tax Reform Act of 1976 was passed, HOAs were no longer required to file Form 1120. Instead, they would file for Form 1120-H.

Who files Form 1120-H?

homeowners association

A homeowners association, or HOA, is either a condominium management association, a residential real estate management association, or a timeshare association. An HOA may elect to file Form 1120-H as its income tax return, in order to take advantage of certain tax benefits.

What type of tax return does an association file?

Generally, an association must file Form 1120-H by the 15th day of the 4th month after the end of its tax year. However, an association with a fiscal year ending June 30 must file by the 15th day of the 3rd month after the end of its tax year.

Do you have to file a tax return for a condo association?

There is a lot of confusion surrounding the taxation of condo associations. Many believe that they are tax-exempt as a “non-profit” and are not required to file a tax return. Even though I have heard this argument over my career, unfortunately, it is simply not correct.

Can a condominium association be a tax exempt organization?

In those cases, both a homeowners’ association and a condominium association sought tax-exempt status, which was denied since the organizations’ activities were for the private benefit of its members, not the public at large.” The IRS has set forth three requirements for any association to meet.

What kind of income does a condo association have?

Most activities of the association will be classified as exempt income (more about this later). But many condo associations will have other income, such as interest income and laundry income, which could subject the entity to a tax liability.

Can a condo association be a 501 ( c ) 4?

It was November 2015 when the IRS made public a letter stating its final determination on whether an unidentified condo qualified for 501 (c) (4) status, which would mean its income would be tax exempt. The IRS denied the request because the condo association didn’t meet the requirements of serving the public good over a sufficiently wide area.