In which circumstance would an auditor be most likely express an adverse opinion?

Andrew Ramirez

Published Feb 19, 2026

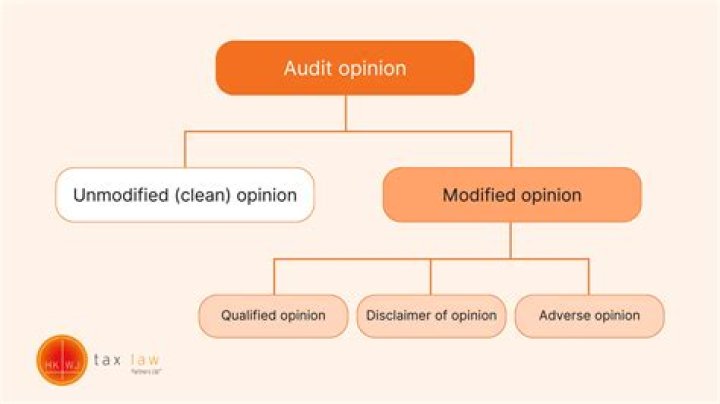

Auditors will usually issue adverse opinions if the financial statements are constructed in a manner that materially deviates from generally accepted accounting principles (GAAP).

What are three circumstances under which an auditor issues a qualified audit opinion?

Without sufficient verification of transactions, an unqualified opinion may not be given. Inadequate disclosures in the notes to the financial statements, estimation uncertainty, or the lack of a statement of cash flows are also grounds for a qualified opinion.

What circumstances will make an auditor qualify his report?

An auditor’s report is qualified when there is either a limitation of scope in the auditor’s work, or when there is a disagreement with management regarding application, acceptability or adequacy of accounting policies. For auditors an issue must be material or financially worth consideration to qualify a report.

In which of the following circumstances would an auditor most likely add an explanatory paragraph to the report while not affecting the auditor’s unqualified opinion?

In which of the following circumstances would auditors most likely add an explanatory paragraph to the standard report without affecting the unqualified opinion on the entity’s financial statements? There is substantial doubt about the entity’s ability to continue as a going concern.

When a client makes extensive use of information technology?

The client’s extensive use of information technology generally would not affect the auditor’s objectives, although it might affect how those objectives are achieved. An audit would express an unmodified opinion with an emphasis-of-matter paragraph added to the report for: A justified change in accounting principle.

What is an emphasis of matter paragraph?

(a) Emphasis of Matter paragraph – A paragraph included in the auditor’s report that refers to a matter appropriately presented or disclosed in the financial statements that, in the auditor’s judgment, is of such importance that it is fundamental to users’ understanding of the financial statements.

Who is a qualified auditor?

qualified auditor means a person who is eligible for appointment as a statutory auditor under Part 42 of the Companies Act 2006; Sample 1.

What is an explanatory paragraph audit?

The explanatory paragraph should include (1) a statement that the previously issued financial statements have been restated for the correction of a misstatement in the respective period and (2) a reference to the company’s disclosure of the correction of the misstatement.

How do you audit beginning balances?

Illustrative Test of Balances Audit Procedures for Opening Balances

- Examine bank-statement reconciliations for the last month of the prior period and the first month of the current period for unusual entries.

- Reconcile the aged trial balance to the general ledger at the end of the prior period.

Is going concern a key audit matter?

If the auditor reports on key audit matters, any material uncertainty related to going concern is by its nature a key audit matter.

Which audit evidence is more reliable?

Audit evidence is more reliable when it exists in documentary form, whether paper, electronic, or other medium (for example, a contempo- raneously written record of a meeting is more reliable than a subse- quent oral representation of the matters discussed). audit evidence provided by photocopies or facsimiles.

What is qualified auditor report?

A qualified audit report is a report issued by an auditor that reports certain discrepancies in the financial statements prepared by the entity. Such report therefore issues a qualified opinion on the true and fair view of the financial position as reported in the financial statements.