How to identify relevant cash flows?

Ava Robinson

Published Feb 20, 2026

In order to get the relevant cash flow, what is required is the incremental revenue – ie the extra revenue that will be earned if the move is made. Thus if the advertising is only in the papers, then the incremental revenue earned will be 40% x $40,000 = $16,000.

How are cash flow based capital expenditure decisions taken in a company?

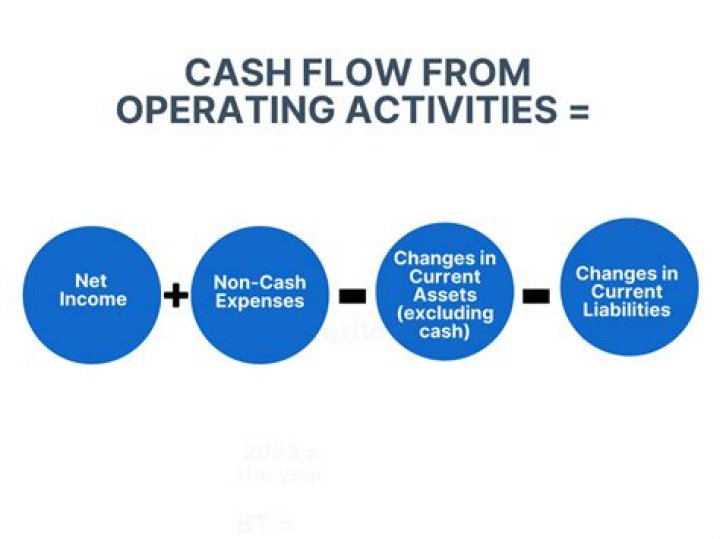

Cash flow from investing activities subtracts capital expenditures from all income generated by these assets. Financing activities records the financing of the company’s operations, including the payment of dividends, the sale or purchase of stock, and the net amount the company has borrowed.

Which of the following should not be included in a project’s incremental cash flows because they are cash outlays that have already been made and have no effect on cash flows relevant to a current decision?

A sunk cost is a cash outlay that has already been made and cannot be recovered. Sunk costs have no effect on the cash flows relevant to the current decision. As a result, sunk costs should not be included in a project’s incremental cash flows.

Is sunk cost a relevant cash flow?

1. Sunk costs (past costs) or committed costs are not relevant. Sunk, or past, costs are monies already spent or money that is already contracted to be spent. A decision on whether or not a new endeavour is started will have no effect on this cash flow, so sunk costs cannot be relevant.

How important is cash flow for project evaluation?

Cash flow analysis is one of the most important pieces of financial information for a firm. Before approving a loan banks analyze the cash flow of firms to decide whether the companies have the ability to repay a loan. They will result in cash outflows (costs). …

What are the relevant incremental cash flows for project evaluation?

The incremental cash flows for project evaluation consist of any or all changes in the firm’s future cash flows that are a direct consequence of taking the project. The relevant cash flows that should be included in a capital budgeting analysis. (So if you start the company with 10 million and gain 15 million.