How much does something have to cost to be depreciated?

Mia Ramsey

Published Feb 28, 2026

Depreciated cost is the value of a fixed asset minus all of the accumulated depreciation that has been recorded against it. In a broader economic sense, the depreciated cost is the aggregate amount of capital that is “used up” in a given period, such as a fiscal year.

Which depreciation method is the best method for a company to use?

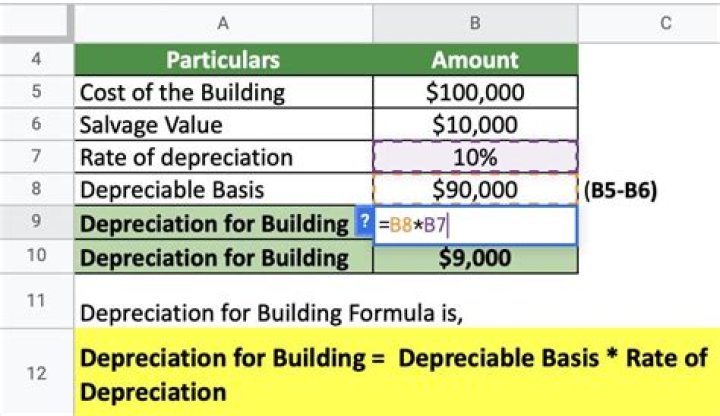

Straight-Line Method: This is the most commonly used method for calculating depreciation. In order to calculate the value, the difference between the asset’s cost and the expected salvage value is divided by the total number of years a company expects to use it.

How do you calculate depreciated cost?

Straight-Line Method

- Subtract the asset’s salvage value from its cost to determine the amount that can be depreciated.

- Divide this amount by the number of years in the asset’s useful lifespan.

- Divide by 12 to tell you the monthly depreciation for the asset.

What are the rules for depreciation for small businesses?

Depreciation rules are established by the IRS and directly affect your business taxes at year’s end.

Why are supplies not considered to be depreciable assets?

Supplies cannot be depreciated because they are considered to be used within a single year and they are expensed during that year. Accounts receivable are not depreciable assets. You begin depreciating an asset when you place it into service. “Placing into service” means that the asset is “ready and available for use.”

Can a business claim depreciation on personal taxes?

The Internal Revenue Service (IRS) has five specific requirements to help businesses determine which of their assets are depreciable. Depreciable property must: You can’t claim depreciation on your personal taxes because depreciation is a form of a business expense.

How often do you have to depreciate an asset?

You can continue to deduct a portion of the asset’s purchase cost every year, until you either stop using the asset, or until you have reclaimed the entire value of the depreciated item. Note that, if you use an asset for both personal and business purposes, you can only depreciate a percentage of the asset’s purchase price.