How many years can losses carry over?

James Craig

Published Mar 04, 2026

If the net amount of all your gains and losses is a loss, you can report the loss on your return. You can report current year net losses up to $3,000 — or $1,500 if married filing separately. Carry over net losses of more than $3,000 to next year’s return. You can carry over capital losses indefinitely.

Which losses can not be carried forward?

The following losses cannot be carried forward unless the return of income (for the year in which the loss is incurred) is submitted within the due date [of submission of return as given in section 139(1)]. loss (not being unabsorbed depreciation etc., from the activity of owning and maintaining race horses.

Can you carry over capital losses?

Capital losses that exceed capital gains in a year may be used to offset ordinary taxable income up to $3,000 in any one tax year. Net capital losses in excess of $3,000 can be carried forward indefinitely until the amount is exhausted.

What happens to capital losses at death?

Use any loss remaining to reduce other income for the year of death, the year before the year of death, or for both years. If you claim any remaining net capital loss in the year of death, you should claim it as a negative amount in brackets at line 12700 of the final return.

When to use capital loss carryover for 2015?

The capital loss carryover from 2014 is what he can use on his 2015 tax return. He should file amended returns for 2012, 2013, and 2014 if there is still a carryover in those years.

Can a tax loss be carried over to the next year?

The gain and the loss would offset each other on your return. You would have no tax loss remaining to carry over to the next year in this situation.

When do you carry forward a loss to the next year?

If you have more in a net loss than the profit in one year, you can carry over the unused NOL to the next carry forward year or a previous year. Then you can begin again at Step 4 until you have carried forward (or carried back) the entire amount of the loss.

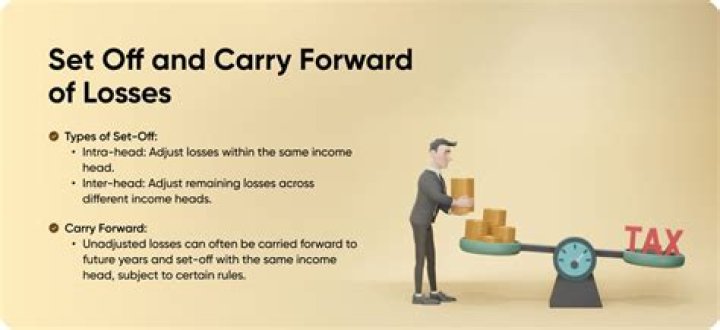

What do you mean by loss carryforward in accounting?

Capital loss carryover is the amount of capital losses a person or business can take into future tax years. Loss carryforward is an accounting technique that applies the current year’s net operating losses to future years’ profits in order to reduce tax liability.