How many years can an S Corp show a loss?

Sarah Duran

Published Feb 16, 2026

The IRS will only allow you to claim losses on your business for three out of five tax years. If you don’t show that your business is starting to make a profit, then the IRS can prohibit you from claiming your business losses on your taxes.

Can I write off S Corp losses?

Assuming you actively participate in the operation of your S corporation and you’re not merely a passive investor, if your S corporation suffers a loss in any tax year you can deduct your share of the loss against your other sources of income, such as dividends, interest, your spouse’s wages, etc.

What if my S Corp has a loss?

If a shareholder has S corporation loss and deduction items in excess of stock basis and those losses and deductions are claimed based on debt basis, the debt basis of the shareholder will be reduced by the claimed losses and deductions.

Can S Corp losses offset personal income?

S corporations are “pass-through” entities, meaning income passes through the corporate structure directly to individual shareholders. As such, losses pass directly to shareholders as well. That means shareholders can use losses in an S corporation to offset their personal income, thus reducing their tax liability.

Do S Corp distributions have to be equal?

The distribution is based on the percentage of stock that each shareholder holds in the corporation. Because S-Corporations may only issue one kind of stock the distribution of the earnings to shareholders should always be proportionate to their holdings in the corporation.

Do S corps get tax refunds?

The S-corp files a Form 1120S and issues a Form K-1 to each shareholder, who then reports the income and pays tax on their individual returns. These individual owners would receive a refund only if their total payments and withholding exceed their total tax liability on the return.

Can an S Corp carry forward losses?

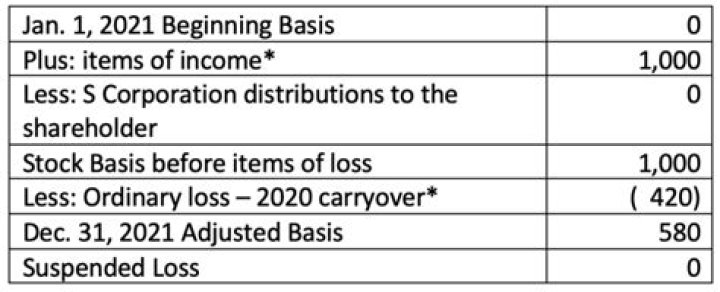

A taxpayer cannot take S corporation losses and deductions on their return to the extent they exceed the sum of their stock and debt basis in the corporation. Losses and deductions in excess of this aggregate amount are suspended and carried forward indefinitely until the basis limitations allow them to deduct them.

How do I report an S Corp distribution?

Use Schedule K-1 to Complete Your Schedule E If you receive distributions from your S corporation, you’ll rely on the information provided on your Form K-1 to report and pay tax on that income. You’ll need to use the information from the K-1 to complete one or more required IRS schedules.

What are S Corp retained earnings?

S Corp retained earnings are the profits made by the business that are retained and not distributed to the shareholders after they have paid taxes on such profits of the business. For that reason, the S Corp must distribute all pre-tax profits to the shareholders for tax purposes.

Do S Corp losses pass through?

An S corporation’s tax items generally pass through to shareholders on a pro rata basis and are reportable by S corporation shareholders in the shareholder’s taxable year in which the S corporation’s year ends.

How are S Corp distributions reported?

If you receive distributions from your S corporation, you’ll rely on the information provided on your Form K-1 to report and pay tax on that income. You attach your Schedule E, along with any other required schedules or forms, to your IRS Form 1040, U.S. Individual Income Tax Return.

Do S corp distributions count as income?

When an S Corporation distributes its income to the shareholders, the distributions are tax-free. Distributions may include amounts that have been taxed in a prior year (as pass-through income), amounts that are taxed in the current year, and/or amounts that have not been taxed at all.

What does Schedule C-profit or loss from business show?

Schedule C – Profit or Loss from Business is part of the individual income tax return IRS Form 1040. It shows the income of a business for the tax year, as well as deductible expenses.

What are short term gains and losses on schedule D?

Short-term gains and losses The initial section of Schedule D is used to report your total short-term gains and losses. Any asset you hold for one year or less at the time of sale is considered “short term” by the IRS.

Are there any changes to small business Schedule C?

The 2017 Tax Cuts and Jobs Act has made several changes to small business taxes that you should know about before you work on this form. If you are having a tax preparer work on your Schedule C, be sure to add these items to your discussion. These changes are all for tax years beginning with 2018. Accounting method.

What happens if a s Corporation loses 100, 000?

This $100,000 loss–the loss will look like a big deduction on the front of the individual’s tax return–should save anywhere between $10,000 and $50,000 of taxes. One common problem exists, however, with deducting S corporation losses.