How long does it take to get an equity line of credit approved?

Andrew Mclaughlin

Published Apr 25, 2026

To get the HELOC, you need equity. If you have enough equity at the time of closing your home purchase, you can get a HELOC in as little as 30 to 45 days, which is the time it takes for loan underwriters to process the application. They use this time to confirm you meet lending requirements for the new debt.

What to know before applying for a HELOC?

The first thing to consider is the HELOC interest rate. A HELOC will have a variable interest rate that goes up and down in relation to an index, like the prime rate. But you’ll also want to consider upfront costs, closing costs and any annual fee.

How is a HELOC paid off?

HELOC repayment When you pay off part of the principal, those funds go back to your line amount. When the draw period ends, you enter the repayment period, where you begin paying back the remaining principal on your HELOC, plus interest.

It can take 2 to 4 weeks from application to closing for a home equity loan or HELOC (Home Equity Line of Credit), depending on the complexity of the loan request.

What is a note for a home equity line of credit?

A home equity line of credit, also known as a HELOC, is a line of credit secured by your home that gives you a revolving credit line to use for large expenses or to consolidate higher-interest rate debt on other loans 1 such as credit cards.

Do you need appraisal for HELOC?

Is an appraisal required with a HELOC? In general, a new appraisal will be required to qualify for a home equity line of credit. However the lender determines a current home value, it’s needed to calculate the amount of credit you’ll be eligible to borrow.

When to apply for a home equity line of credit?

Especially now—if you’ve lost your job because of the coronavirus, need cash, and have equity in your home—taking out a HELOC may be a good option. Many banks are still offering them, though Wells Fargo and JPMorgan Chase were two frontrunners that announced application freezes for new HELOCs in the spring of 2020.

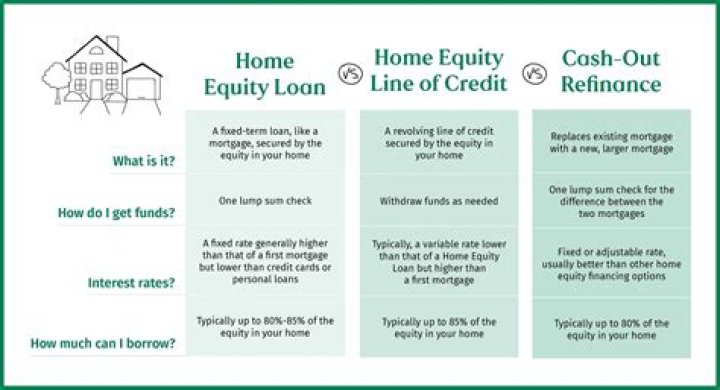

What’s the difference between a home equity loan and a HELOC?

A home equity loan comes as a lump sum of cash, often with a fixed interest rate. Home equity lines of credit (HELOC) are a revolving source of potential funds, much like a credit card, that you use as you see fit with a variable interest rate. Banks underwrite second mortgages much like other home loans.

What happens if an ex spouse uses a home equity line of credit?

If the lender ever wants to enforce the loan terms and foreclose on the home, the lender will need to have all owners at the time the loan was taken out sign the mortgage, trust deed or other document that creates a lien on the home. You should go back and determine when the loans were taken out and make sure you were either on title or off title.

When do I withdraw money from my home equity line?

Ask how you can spend money from the credit line — with checks, credit cards, or both. You should find out if your home equity plan sets a fixed time — a draw period — when you can withdraw money from your account. Once the draw period expires, you may be able to renew your credit line.