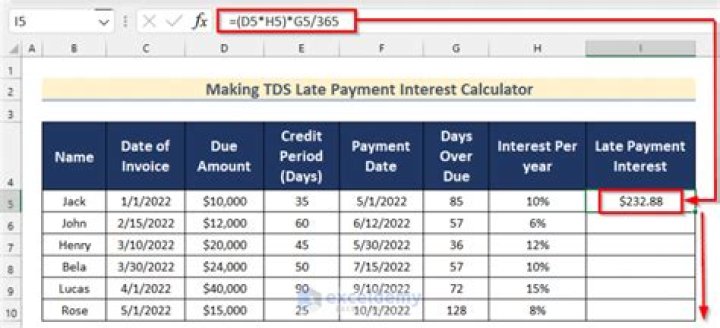

How is interest on late payment of TDS calculated?

Andrew Ramirez

Published May 15, 2026

Interest on Late Deduction = 12300 * 2 months * 1/100 = 246. Under Section 201(1A), you will have to pay interest of 1.5% per month or part of the month, from the Date of Deduction(of TDS) to the Date of Payment.

What is interest on late payment of income tax?

Interest under section 234A is levied for delay in filing the return of income. Interest is levied at 1% per month or part of a month. The nature of interest is simple interest. In other words, the taxpayer is liable to pay simple interest at 1% per month or part of a month for delay in filing the return of income.

Is late filing fees disallowed under income tax?

Late fee is not paid for a purpose which is an offence or prohibited. Hence, it will be allowed under Section 37 as it is is not an offence or prohibited under any law. Therefore, late fees paid for delay in filing GST returns will be allowed as a deduction under Income Tax.

Is interest on TDS penalty?

Interest in such a case will be levied at 1% for every month or part of the month. Every deductor has to furnish quarterly statement in respect of tax deducted by him i.e., TDS return. As per section 201(1A), interest for delay in payment of TDS should be paid before filing the TDS return.

What is interest rate on TDS late deposit?

Under Section 201(1A), in case off late deposit of TDS after deduction, you have to pay interest. Interest is calculated at the rate of 1.5% per month from the date on which TDS was deducted to the actual date of deposit.

Is interest on late payment of GST allowed as deduction?

Any tax, duty, cess or fee paid under any law in force is allowed as a deduction when it is paid- this includes GST, customs duty or any other taxes or cesses paid. Interest paid on these taxes are also eligible for deduction.

How is TDS interest and penalty calculated?

TDS interest for late payment For example, say the payable TDS amount is Rs 5000 and the date of the deduction is 13th January. TDS payment date for that deduction is on 17th May. Then the interest payable is Rs 5000 x 1.5% p.m. x 5 months = Rs 375 (from the month of January to the month of May).