How does the 962 election work?

John Thompson

Published Apr 05, 2026

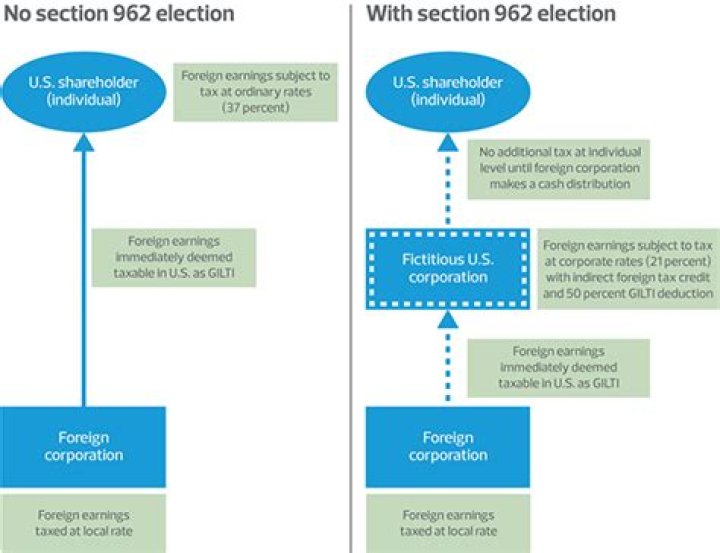

962 allows an individual U.S. shareholder to make an annual election to be taxed as a C Corporation on certain specific income earned by its foreign subsidiary (including GILTI). By making this election, the shareholder may claim an indirect foreign tax credit for foreign taxes the corporation paid.

Can a 962 election be made on an amended return?

In addition, the Section 962 election can be made retroactively through an amended tax return. Furthermore, if the Japanese corporation’s earnings are subject to a high foreign tax then GILTI can be excluded from the individual’s U.S. federal income tax return.

Can a trust make a 962 election?

The election under section 962 may be made only by an individual (including a trust or estate) who is a United States shareholder (including an individual who is a United States shareholder because, by reason of section 958(b), he is considered to own stock of a foreign corporation owned (within the meaning of section …

Is foreign branch income eligible for Fdii?

The Final Regulations include a definition of “foreign branch income” for FDII purposes that is fully consistent with the definition in the final foreign tax credit regulations issued in 2019. This is significant because foreign branch income cannot be gross FDDEI.

Can US source income be Subpart F?

In the case of a controlled foreign corporation, subpart F income does not include any item of income from sources within the United States which is effectively connected with the conduct by such corporation of a trade or business within the United States unless such item is exempt from taxation (or is subject to a …

Does Gilti apply to individuals?

The GILTI rules apply to C corporations, S corporations, partnerships and individuals. In addition, U.S. corporate shareholders may also claim an indirect foreign tax credit for 80 percent of the foreign tax paid by the shareholder’s CFCs that is determined to be allocable to GILTI income.

Can an S Corp have foreign income?

Foreign taxes paid by an S corporation pass through to shareholders who can elect to treat them as deductions or credits on their individual returns ( Code Sec. 1373). An S corporation is treated as a partnership rather than a corporation.

What is the difference between Fdii and Gilti?

Foreign Derived Intangible Income (FDII) is a special category of earnings that come from the sale of products related to intellectual property (IP). Global Intangible Low Tax Income (GILTI) is a special way to calculate a U.S. multinational company’s foreign earnings to ensure it pays a minimum level of tax.

Can you make a section 962 election on an amended return?

Who is subject to Gilti income?

Global intangible low-taxed income, called GILTI, is a category of income that is earned abroad by U.S.-controlled foreign corporations (CFCs) and is subject to special treatment under the U.S. tax code.1 The U.S. tax on GILTI is intended to prevent erosion of the U.S. tax base by discouraging multinational companies …

In addition, the Section 962 election can be made retroactively through an amended tax return.

When does a foreign corporation pay tax under section 962?

Thus, when a foreign corporation makes a distribution to a United States shareholder who has made a section 962 election, the individual may pay tax at normal ordinary income rates but only on the amount of the distribution that exceeds the amount of tax previously paid as a result of the section 962 election.

How is GILTI taxed under section 962?

Under section 962, the individual will generally pay tax on his or her pro rata share of GILTI as if he or she were a U.S. corporation. Thus, the reduced corporate rate of 21 percent will apply and the individual may claim an indirect credit with respect to any foreign taxes that the foreign corporation has paid.

What is the maximum tax credit under section 962?

A Section 962 election permits individual CFC shareholders to pay a maximum of 21 percent on subpart F inclusions. It also allows individual CFC shareholders the ability to offset their subpart F liability with foreign tax credits for taxes paid by the CFC.

When to apply final regulations under section 962?

US Shareholders making Section 962 elections may choose to apply the Final Regulations to a foreign corporation’s tax years beginning on or after 1 January 2018, and to the US Shareholder’s tax year in which or with which the foreign corporation’s tax year ends. 8