How does an operating lease affect the income statement?

Henry Morales

Published Feb 17, 2026

An operating lease is treated like renting—lease payments are considered as operating expenses. Assets being leased are not recorded on the company’s balance sheet; they are expensed on the income statement. So, they affect both operating and net income.

How does IFRS 16 impact income statement?

IFRS 16 is expected to change the balance sheet, income statement and cash flow statement for companies with material off balance sheet leases. The accounting requirements for lessors are substantially unchanged. Disclosure is enhanced. IFRS 16 does not change substantially how a lessor accounts for leases.

Does IFRS 16 affect net income?

The overall impact on the net profit is the same under IFRS 16 and IAS 17, however, with the application of the right-of-use model the presentation of lease payments in the statement of comprehensive income will change.

How do you treat an operating lease valuation?

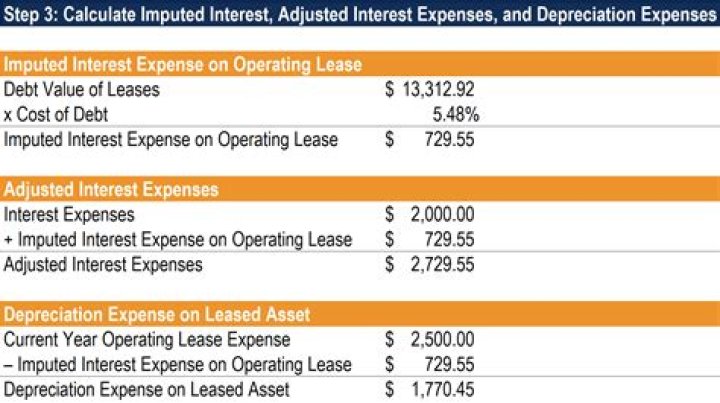

The operating lease expenses after year 5 are treated as an annuity. The present value of operating leases can be treated as the equivalent of debt. The capitalization of operating leases increases the book value of capital substantially. There is no effect on the book value of equity.

Why is IFRS 16 better than IAS 17?

IAS 17 – Disclosures cover the specific requirement of finance leases separate from operating leases. IFRS 16 – Disclosures do away with the separate presentation of finance and operating leases for lessees and instead requires disclosures of the right of use assets and liabilities.

What is the impact and effect of IFRS 16 on financial statements? The introduction of IFRS 16 / AASB 16 will lead to an increase in leased assets and financial liabilities on the balance sheet of the lessee. Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA) of the lessee increases as well.

What are the impacts of IFRS 16 leases?

IFRS 16 impacts the lessee’s P&L where they have previously classified leases as operating leases. The lease expense recognised under IAS 17 will now be recognised as depreciation of the right-of-use asset to be recognised on the balance sheet as well as an interest expense.

Does IFRS 16 impact net income?

How does operating lease expense affect free cash flow?

There are two effects on free cash flow to the firm (FCFF) when we treat operating lease expenses as financing expenses by capitalizing them: FCFF will increase because the imputed interest expense on the capitalized operating leases is added back to the operating income (EBIT).

How to adjust operating income for operating lease?

First, we need to adjust operating income. Begin with the reported operating income (EBIT). Then, add the current year’s operating lease expense and subtract the depreciation on the leased asset to arrive at adjusted operating income.

How are lease payments recorded on the balance sheet?

An operating lease is treated like renting—lease payments are considered as operating expenses. Assets being leased are not recorded on the company’s balance sheet; they are expensed on the income statement. So, they affect both operating and net income. Other characteristics include:

How is a rental expense classified in an operating lease?

A company that leases an asset under the operating lease arrangement must classify each lease payment as a rental expense by debiting its rental expense account and crediting its lease payable account.