How does a spouse inherit an IRA?

James Craig

Published Mar 31, 2026

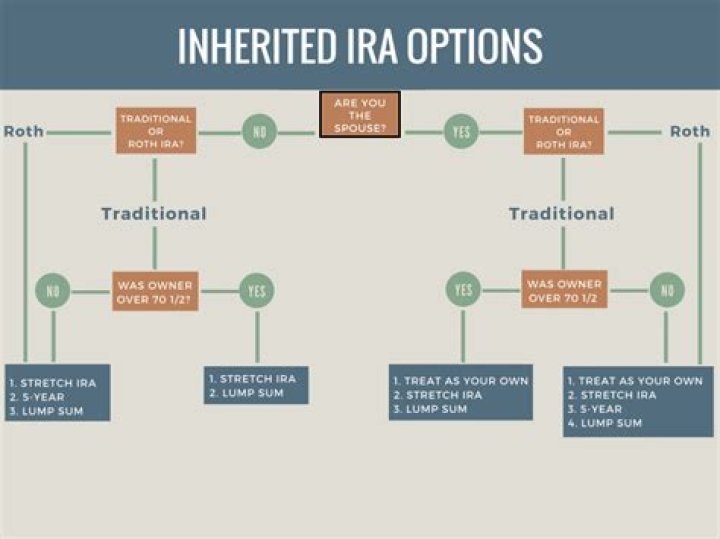

If a traditional IRA is inherited from a spouse, the surviving spouse generally has the following three choices: Treat it as his or her own IRA by designating himself or herself as the account owner.

If you inherit a Traditional, Rollover, SEP, or SIMPLE IRA from a spouse, you have several options, depending on whether your spouse was under or over age 72. Most commonly, those who inherit an IRA from a spouse transfer the funds to their own IRA.

What can be done with an inherited IRA?

The IRS doesn’t allow you to roll the money from an inherited IRA into one of your existing accounts. Instead, you’ll have to transfer your portion of the assets into a new IRA set up and formally named as an inherited IRA; for example, (Name of Deceased Owner) for the benefit of (Your Name).

What happens to the value of an IRA when a spouse dies?

The entire fair market value of the IRA or 401 (k) would be included in the value of the deceased owner’s estate for estate tax purposes if the account was left to anyone other than a surviving spouse.

Can a surviving spouse change the beneficiary of an IRA account?

The surviving spouse won’t be able to change the beneficiary of the account after the surviving spouse dies, however. Spouses can leave assets to each other at death free from estate taxation due to the unlimited marital deduction provided for under the federal tax code.

Can you take control of an IRA after a loved one dies?

Anyone can take control of an IRA or 401 (k) after a loved one dies by simply presenting the original death certificate to the bank or financial institution where the account is held. The only requirement is that the individual be named as the beneficiary.

When to take RMD on deceased spouses IRA?

Delay RMD’s until your deceased spouse would have been 70 and 1/2 (when the IRA would have been subject to RMD’s anyway). If you’re older than your deceased spouse was, the required minimum distributions are based on their IRS Single Life Expectancy table.