How does a newly formed partnership handle the contribution of previously depreciated assets?

James Craig

Published Mar 31, 2026

starts over, using the contributed value as the new cost basis does not depreciate the contributed asset continues the depreciation life as if the owner had not changed shortens the useful life of the asset per the partnership agreement.

Do you depreciate fixed assets?

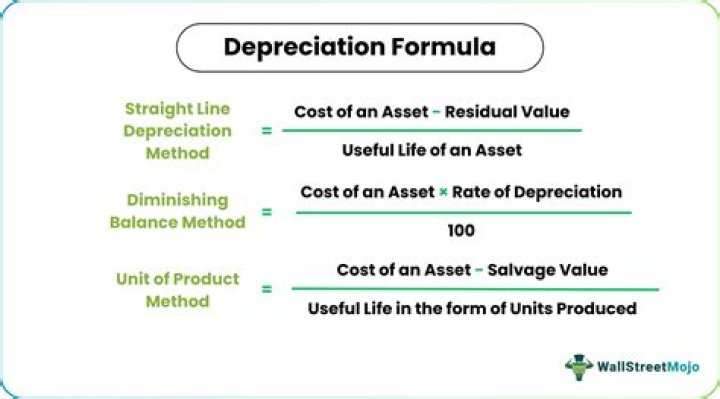

Depreciation is the systematic reduction of the recorded cost of a fixed asset. Examples of fixed assets that can be depreciated are buildings, furniture, and office equipment. The only exception is land, which is not depreciated (since land is not depleted over time, with the exception of natural resources).

Can you take bonus depreciation on contributed property?

Property contributed to a partnership is not eligible for bonus depreciation, whether or not the tax basis of the property equals the property’s fair market value. While the purchaser is able to use bonus depreciation to any eligible property deemed acquired, the partnership to which they are contributed cannot.

What is the basis of property contributed to a partnership?

The basis of property contributed to a partnership by a partner shall be the adjusted basis of such property to the contributing partner at the time of the contribution increased by the amount (if any) of gain recognized under section 721(b) to the contributing partner at such time.

Fixed assets, such as equipment and vehicles, are major expenses for any business. After a certain period of time, these assets become obsolete and need to be replaced. Assets are depreciated to calculate the recovery cost that is incurred on fixed assets over their useful life.

What is the preferred method of resolving a partner’s deficit balance according to the Uniform Partnership Act?

B. Frequent reporting by the accountant is rarely necessary. What is the preferred method of resolving a partner’s deficit balance, according to the Uniform Partnership Act? The partner with a deficit balance must contribute personal assets to cover the deficit balance.

When do you contribute a depreciable asset to a partnership?

Yes, when you contribute a depreciable asset to a partnership, your basis, in-service date, and accumulated depreciation carry over to the partnership. The partnership continues to use the depreciation method and remaining depreciable life used by the contributing partner.

How is depreciation of fixed assets related to earnings?

Depreciation of fixed assets is an accounting term that is used to represent how much of an asset’s value has been used up over time. Depreciation is, therefore, a calculated expense, which leads to a decrease in earnings. Depreciation can be related to: physical wear and tear, linked with time,

How do I report depreciation for property contributed by?

LLC books depr schedule assets at original cost and accumulated depr accounts balances. Then the fair market (or agreement price) value minis the net book value of depr schedule is booked as a non-depr asset like land. Yes original dates can normal be entered in most software.

What is the tax basis of a LLC?

Under Sec. 723, the LLC’s basis in the contributed assets is the same as each contributing member’s basis in the assets prior to the contribution. Therefore, ABC has a tax basis balance sheet reflecting $16,000 cash, a tax library with a $3,000 tax basis, and computer equipment with an $8,000 tax basis.