How does a corporation elects S corporation status?

Sarah Duran

Published Mar 04, 2026

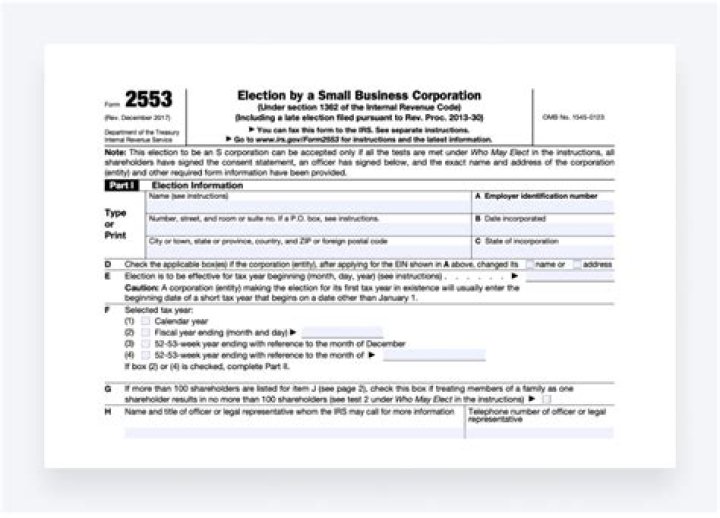

Use IRS Form 2553 to file this election. Form 2553- Election by a Small Business Corporation provides the IRS with detailed information about the corporation requesting S corp status and about the corporation’s eligibility for electing this status.

When is the deadline to elect a s-Corp?

You consent to our cookies if you continue to use our website. The deadline to elect S-Corporation tax treatment depends on whether your business is newly incorporated or is in its second (or later) tax year.

When does a LLC elect to be taxed as a corporation?

The entity normally files the election to be taxed as a corporation on Form 8832, Entity Classification Election , in accordance with Regs. Sec. 301.7701-3(c). However, if an LLC that is eligible to elect S status timely files an S election (Form 2553), the entity is considered to have elected to be taxed as a corporation (Regs.

Who is responsible for late filing of S Corp?

The company’s president, executive officer, or someone in a similar position, neglected to file on time. In some cases, this may also be the corporation’s accountant who failed to file an S-Corp election. The corporation or the shareholders did not know that advanced filing was required — or that they needed to file at all.

When does a C Corporation become a S corporation?

When a C corporation elects to become an S corporation, S status begins on the day following the last day of the electing C corporation’s tax year. For an existing C corporation that is converting to S status, the S election may be filed:

How to elect a LLC as a S corporation?

A timely filed Form 2553 will constitute a deemed entity classification election, as if Form 8832 were filed. However, this deemed entity classification election is effective only if the electing entity meets all of the requirements to be an S corporation.

How to elect tax treatment as a S corporation?

Once it has elected to be taxed as a corporation, it can file a Form 255 3, Election by a Small Business Corporation, to elect tax treatment as an S corporation. If you need help with S Corporation elections, you can post your legal need on UpCounsel’s marketplace.

How does a small business become a S corporation?

In order to become an S corporation, the corporation must submit Form 2553 Election by a Small Business Corporation signed by all the shareholders. See the Instructions for Form 2553 PDF for all required information and to determine where to file the form.

What are the qualifications for S corporation status?

Corporations Qualified to Elect S Corporation Status. The IRS has 8 qualifications for S Corporation status, including: It must be a domestic (U.S.) corporation, with no foreign investors; It must have no more than 100 shareholders; It has only one class of stock; It must use a December 31 year-end.

How are the shareholders of a corporation elected?

The final section asks you to list all the shareholders who must consent to the election, with the number or percent of shares owned, date acquired, and tax year of each shareholder. Each shareholder must also sign and date the form. Part II includes questions about the corporation’s tax year.

Who are the members of a S corporation?

There are some restrictions on who can form an S corporation. You can elect S-corporation status if: The owners are U.S. citizens or residents with valid Social Security numbers You are the single member in an LLC, considered a disregarded entity There are two or more members in your LLC, considered a partnership

When to file Form 2553 for S corporation?

If the entity plans to make the election to be treated as a corporation and become an S corporation on the same date, only Form 2553 is filed, and it should conform to the S corporation rules. The authors recommend that the Form 2553 be filed by the earlier of 75 days or two months and 15 days after the date the S election is to become effective.

When is the effective date of an S corporation?

To conform to the S corporation rules, however, the effective date of the S election should not occur before the earliest date that the LLC has members, acquires assets, or begins conducting business.