How does a company decide on method of depreciation?

Andrew Mclaughlin

Published Feb 16, 2026

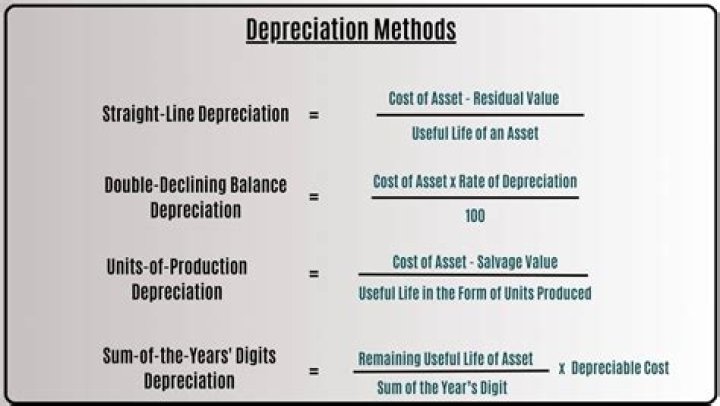

Straight line depreciation is often chosen by default because it is the simplest depreciation method to apply. You take the asset’s cost, subtract its expected salvage value, divide by the number of years it’s expect to last, and deduct the same amount in each year.

Which depreciation method is the best method for a company to use?

The Straight-Line Method This method is also the simplest way to calculate depreciation. It results in fewer errors, is the most consistent method, and transitions well from company-prepared statements to tax returns.

WHO calculates depreciation?

Three Main Methods of Calculating Depreciation The IRS has information about the depreciation and lifespan of assets.

Why do companies change depreciation methods?

You are most likely to request a change to a depreciation method because you revise the estimated future benefits afforded by the asset or gain more information about the consumption pattern of the asset. A fixed asset’s carrying value bears no necessary relationship to its market value.

Can I change the method of depreciation?

At the end of each financial year, management should review the method of depreciation. Also, the justification and financial effects of the change needs to be disclosed. Thus, the method of depreciation can be changed without retrospective effect or with retrospective effect.

How do you correct depreciation not taken?

Form 3115, Change in Accounting Method, is used to correct most other depreciation errors, including the omission of depreciation. If you forget to take depreciation on an asset, the IRS treats this as the adoption of an incorrect method of accounting, which may only be corrected by filing Form 3115.

What are the method of changing depreciation?

Concept And Accounting of Depreciation

- Change in Method of Depreciation.

- Profit or Loss on Disposal of Asset.

- Sinking Fund Method.

- Annuity Method.

- Units of Production Method.

- Diminishing Balance Method.

- Straight Line Method.

- Cost of Assets for Calculating Depreciation.

Who decides depreciation?

The Income Tax Officer also has the right to determine the proportionate part of the depreciation under Section 38 of the Act. Co-owners can claim depreciation to the extent of the value of the assets owned by each co-owner. You cannot claim depreciation on the cost of land. Depreciation is mandatory from A.Y.

Which depreciation method do most companies use?

straight-line method

Businesses can recover the cost of an eligible asset by writing off the expense over the course of its useful life. The straight-line method is the simplest and most commonly used way to calculate depreciation under generally accepted accounting principles.

Can a company change its method of depreciation?

Thus, the method of depreciation can be changed without retrospective effect or with retrospective effect. Without retrospective effect means no adjustment will be made for past entries and only in the future depreciation shall be charged by the new method.

Do all fixed assets have to be depreciated?

Which Asset Does Not Depreciate? All depreciable assets are fixed assets but not all fixed assets are depreciable. For an asset to be depreciated, it must lose its value over time. For example, land is a non-depreciable fixed asset since its intrinsic value does not change.

Which is depreciation method does company a use?

Companies A and B purchase a similar machine at the same time and for the same cost. In reporting this acquisition, company A uses the straight-line method of depreciation, while company B uses the double declining balance method. Other than the choice of depreciation method, both companies use similar estimates and assumptions.

What’s the best way to depreciate an asset?

Some of the more common depreciation methods include straight line, sum-of-the-years digit and declining balance depreciation. Depending on the method chosen, depreciation for a particular asset could be more during the beginning years and less thereafter. The method chosen will have an impact on profits for that particular period.

How does the straight line depreciation method work?

The straight-line depreciation method calculates depreciation based on the asset’s price of purchase, its salvage value and its useful life. An asset’s salvage value is how much this asset is worth after its useful life has ended. This value can be a positive number, zero or a negative number.

How is the percentage of depreciation calculated?

This is similar to the straight line method. First you calculate the percentage of depreciation in the straight line method by taking the depreciation base ($10,000 – $700 = $9,300) and dividing it by $3,100, which is the yearly depreciation expense in the first method, to get 33.33 percent. This percentage is then doubled to get 66.66 percent.