How do you find the equivalent units of production for FIFO?

Andrew Ramirez

Published Feb 19, 2026

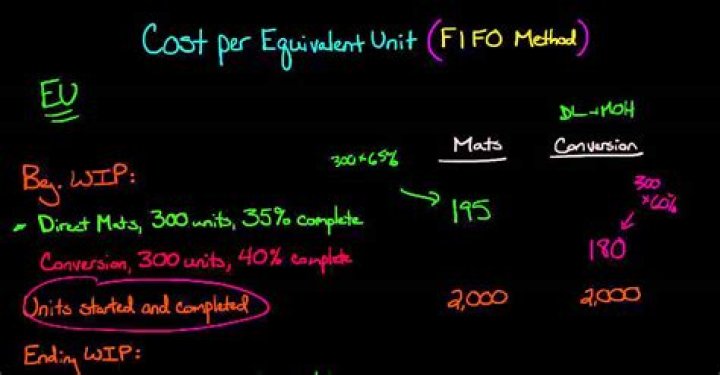

In this example we will use the equivalent units FIFO method in which case the two variables used in the formula are defined as follows:

- Production cost = Costs added during the period.

- Equivalent units = Beginning WIP units (% to complete) + Started and completed units (100%) + Ending WIP units (% to completed)

How do you find the equivalent units of production?

Equivalent units. are calculated by multiplying the number of physical (or actual) units on hand by the percentage of completion of the units. If the physical units are 100 percent complete, equivalent units will be the same as the physical units.

What is an equivalent unit of production?

What is Equivalent Units of Production? It is the number of completed units of an item that a company could theoretically have produced, given the amount of direct materials, direct labor, and manufacturing overhead costs incurred during that period for the items not yet completed.

What is the formula for calculating units of production depreciation?

The units of production method requires a two-step process: Step 1: Calculate Depreciation per Unit: Depreciation per unit=(Cost−Salvage)expected number of units over lifetime.

How do you calculate equivalent units of production?

Equivalent units of production is a term applied to the work-in-process inventory at the end of an accounting period. In short, if 100 units are in process but you have only expended 40% of the processing costs on them, then you are considered to have 40 equivalent units of production.

What is the number of FIFO equivalent units?

Equivalent units under FIFO method of process costing are the number of finished units that could have been prepared in a process during a period had there been no unfinished units, either in opening WIP or closing WIP.

How are equivalent units of production converted in FIFO?

Second, the FIFO method gives full consideration to the amount of processing done during the current period on the units in beginning inventory and on the units in ending inventory. In FIFO, both beginning and ending inventories are essentially converted to an equivalent units basis.

How is work in process calculated in FIFO?

Work in Process completed + units started and completed + units in Ending Work in Process Beg. Work in Process Costs + Costs added this period Beg. Work in Process Costs + Equivalent Units x cost per equivalent unit for units finished from Beg. Work In Process, Units started and completed and units in End. Work In Process

How does the weighted average method differ from the FIFO method?

The weighted average method blends the cost and work of the current period with the cost and work of the previous period. The FIFO method, on the other hand, clearly spares the work done in current period and the work done in prior period. The equivalent units of production under FIFO method include work done in the current period only.

How are beginning and ending inventories converted to equivalent units?

In FIFO, both beginning and ending inventories are essentially converted to an equivalent units basis. The equivalent units belonging to beginning inventory represent the work done during the current period to complete the units that were not completed in the previous period.