How do you count the 60 days in a 60 day rollover?

Emma Jordan

Published Mar 28, 2026

You do NOT start counting the 60 days from the date you request the distribution, the date on the check, or the date the funds left the IRA account. You start counting the days on the date you receive the funds if they are mailed, or the date they hit your bank account if they are transferred.

Does the 60 day rule apply to direct rollovers?

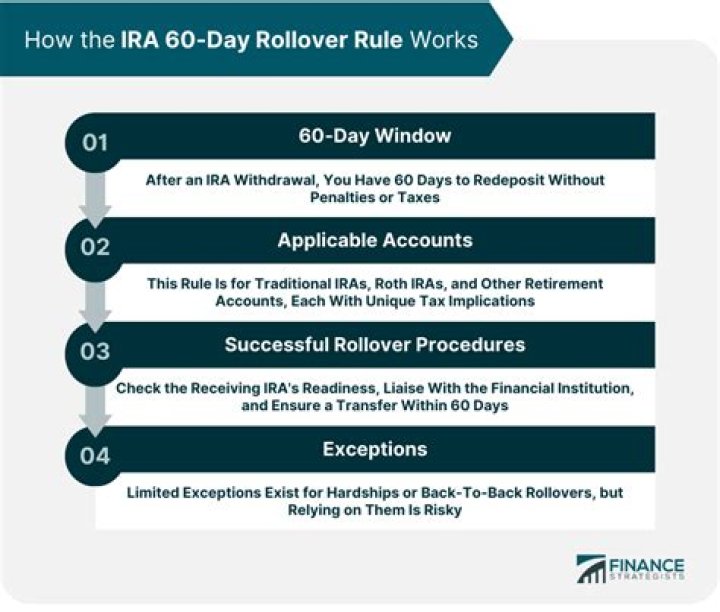

You have 60 days from the date you receive an IRA or retirement plan distribution to roll it over to another plan or IRA. The IRS may waive the 60-day rollover requirement in certain situations if you missed the deadline because of circumstances beyond your control.

Does a 60 day rollover include weekends?

The 60-day period is measured in calendar days, not business days. The IRS has approved private letter rulings requesting extra time for rollovers when the 60th day falls on a weekend. However, your best plan is to not wait until the last minute. During the 60-day period, you may do what you like with your funds.

Can a 60 year old take money out of an IRA?

Once you reach the age of 60, you can breathe a sigh of relief. You’ve outlived traditional IRA early withdrawal penalties and restrictions established by the Internal Revenue Service. And if you own a traditional IRA, you haven’t yet seen the boom of required minimum distributions come crashing down.

How old do you have to be to contribute to an IRA?

Other IRA Age Rules to Consider. While there are maximum age limits for some IRAs, you can begin contributing to traditional, Roth and SIMPLE IRAs at any age. Only SEP IRAs require participants be at least 21 years of age.

When do I have to report my IRA withdrawals?

All IRA withdrawals must be reported on your taxes. IRA stands for individual retirement account. Tax-deferred IRAs, including traditional IRAs, SEP IRAs and SIMPLE IRAs, allow qualified withdrawals to be taken any time after age 59 1/2.

How old do you have to be to contribute to a SEP IRA?

Only SEP IRAs require participants be at least 21 years of age. For each of these accounts, your contributions must not exceed the amount of taxable income you earn that year. There may be other eligibility terms, but your youth won’t hold you back from putting money away for your future.