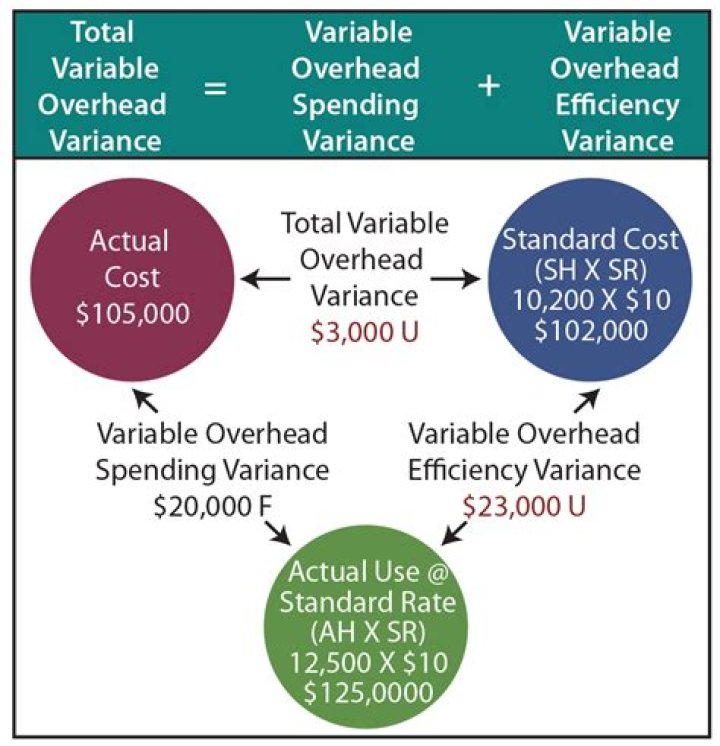

How do you calculate variable overhead spending variance?

James Craig

Published Feb 19, 2026

Solution:

- Variable overhead spending variance = (Actual hours worked × Actual variable overhead rate) – (Actual hours worked × Standard variable overhead rate)

- *Actual hours worked × Actual variable overhead rate = Actual variable overhead for the period.

- Variable overhead spending variance = AH × (AR – SR)

How is spending variance calculated?

The spending variance for direct materials is known as the purchase price variance, and is the actual price per unit minus the standard price per unit, multiplied by the number of units purchased. The variance calculation is normally applied to each individual line item within this general category of expense.

What causes variable overhead rate variance?

The variable overhead efficiency variance is driven by the difference between the actual hours worked and the standard hours expected for the units produced. The other is caused by actual production being above or below the expected production level.

What is included in variable overhead?

Variable overhead is the cost of operating a business, which fluctuates with manufacturing activity. As production output increases or decreases, variable overhead moves in tandem. Examples of variable overhead include production supplies, utilities for the equipment, wages for handling, and shipping of the product.

What does a favorable labor rate variance indicate?

A favorable labor rate variance indicates that the standard labor rate is greater than the actual labor rate.

How much does a variance cost?

The zoning examiner may then hold a hearing to determine if the variance should be granted. How much does a property variance cost? Each application for a variance costs $1000, which includes a $500 initial appeal deposit.

How is DM price variance calculated?

The formula for this variance is:(standard price per unit of material × actual units of material consumed) – actual material cost. (standard price per unit of material × actual units of material consumed) – actual material cost.