How do you calculate useful life of depreciable assets?

Andrew Ramirez

Published May 17, 2026

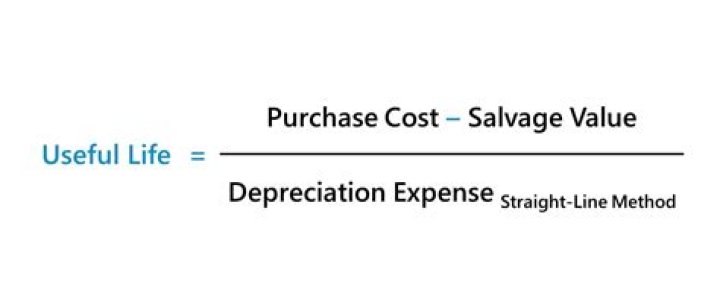

Straight-Line Method

- Subtract the asset’s salvage value from its cost to determine the amount that can be depreciated.

- Divide this amount by the number of years in the asset’s useful lifespan.

- Divide by 12 to tell you the monthly depreciation for the asset.

What are the major factors that determine the economic life of an asset?

The economic life of an asset is the period of time during which it remains useful to its owner. Financial considerations required for calculating the economic life on asset include its cost at the time of purchase, the amount of time an asset is used in production, and existing regulations pertaining to it.

How do you determine the life of an asset?

How to determine the useful life of an asset. Most commonly, the depreciation of assets is calculated by dividing the cost of the asset by the estimated number of years in its life.

What is asset useful life?

The useful life of an asset is an accounting estimate of the number of years it is likely to remain in service for the purpose of cost-effective revenue generation. The Internal Revenue Service (IRS) employs useful life estimates to determine the amount of time during which an asset can be depreciated.

What is the definition of the class life of an asset?

The useful life of a type of property as defined by the Alternative Depreciation System or the General Depreciation System.

What is the useful life for a building?

Furniture: 5-12 years. Machinery and equipment: 3-20 years. Property, buildings and renovations: 10-50 years.

What do you need to know about MACRS depreciation?

The MACRS tax depreciation system was intended to encourage investors to invest in depreciable assets by allowing large tax savings in the initial years of the asset’s life. Taxpayers can apply MACRS depreciation to various asset classes such as automobiles, office furniture, construction machinery, farm buildings,…

Where does the MACRS asset life table come from?

The MACRS Asset Life table is derived from Revenue Procedure 87-56 1987-2 CB 674. The table specifies asset lives for property subject to depreciation under the general depreciation system provided in section 168 (a) of the IRC or the alternative depreciation system provided in section 168 (g).

How is the recovery period determined for MACRS?

A specific recovery period (the number of years you can claim a deduction) is defined for each class of property. Use the MACRS Depreciation Methods Table (in IRS Pub 946 or Section below) to figure out the class of your asset.

Which is the best method to calculate MACRS?

There are four main ways to calculate depreciation which are GDS using 200% DB, GDS using 150% DB, GS using SL, and ABS using SL. These can be easily understood by breaking down each type below: This stands for general depreciation and declining balance, which is essential for calculating MACRS.