How do you calculate the expected risk of a portfolio?

Andrew Ramirez

Published Feb 16, 2026

Portfolio risks can be calculated, like calculating the risk of single investments, by taking the standard deviation of the variance of actual returns of the portfolio over time.

How do you calculate expected return and risk of a portfolio?

The expected return of a portfolio is calculated by multiplying the weight of each asset by its expected return and adding the values for each investment. For example, a portfolio has three investments with weights of 35% in asset A, 25% in asset B, and 40% in asset C.

What is expected return and risk?

Risk refers to the possibility of the actual return varying from the expected return, ie the actual return may be 30% or 10% as opposed to the expected return of 20%. The risk-free return is the return required by investors to compensate them for investing in a risk-free investment.

What is risk/return portfolio?

The risk of a two-asset portfolio is dependent on the proportions of each asset, their standard deviations and the correlation (or covariance) between the assets’ returns. As the number of assets in a portfolio increases, the correlation among asset risks becomes a more important determinate of portfolio risk.

What is minimum portfolio risk?

Definition: A minimum variance portfolio indicates a well-diversified portfolio that consists of individually risky assets, which are hedged when traded together, resulting in the lowest possible risk for the rate of expected return.

How do you interpret portfolio risk?

A portfolio with a high beta means you may be risking more than you think you are. If your portfolio has a beta of 1.5, and the market falls 10%, your portfolio would be expected to fall 15%. Value at risk (VaR) is used to calculate the maximum loss a portfolio can be expected to lose in a given period.

What is my portfolio value?

Portfolio Value means the value of Your Portfolio (ignoring the annual management charge for the relevant Calculation Period and any accrued but unpaid annual management charges from previous Calculation Periods) as at the end of that Calculation Period; and.

How do you compare risk and return?

The firm must compare the expected return from a given investment with the risk associated with it. Higher levels of return are required to compensate for increased levels of risk. In other words, the higher the risk undertaken, the more ample the return – and conversely, the lower the risk, the more modest the return.

Is the expected return on a portfolio the same as the risk return?

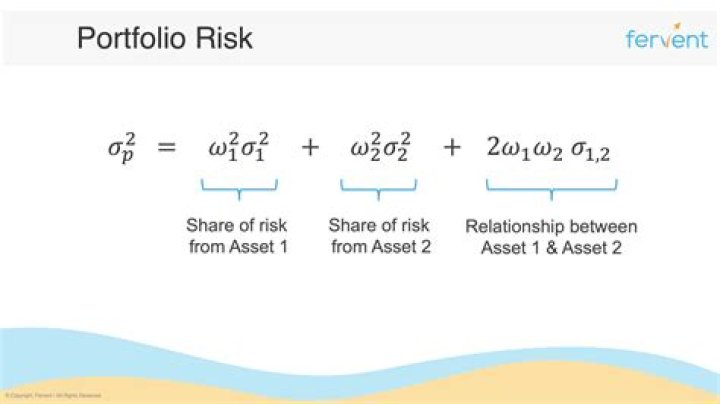

Unlike the expected return on a portfolio which is simply the weighted average of the expected returns on the individual assets in the portfolio, the portfolio risk, σp is not the simple, weighted average of the standard deviations of the individual assets in the portfolios.

How is the return on a portfolio calculated?

∴ Portfolio return is 12.98%. The risk of a security is measured in terms of variance or standard deviation of its returns. The portfolio risk is not simply a measure of its weighted average risk. The securities consisting in a portfolio are associated with each other.

How is the overall risk of a portfolio measured?

In fact, the overall risk of the portfolio includes the interactive risk of asset in relation to the others, measured by the covariance of returns. Covariance is a statistical measure of the degree to which two variables (securities’ returns) move together.

How is the return and risk of a stock determined?

The parameters of the risk and return of any stock explicitly belong to that particular stock, however, the investor can adjust the return to risk ratio of his/ her portfolio to the desired level using certain measures. One such measure is to adjust the weights of the stocks in the investors’ portfolio.