How do you calculate overhead cost based on direct labor hours?

Henry Morales

Published Feb 16, 2026

To calculate the plantwide overhead rate, first divide total overhead by the number of direct labor hours used to find the overhead per labor hour. Next, multiply the overhead per labor hour by the number of labor hours used to produce each unit.

What is the predetermined overhead rate per direct labor hour?

The predetermined overhead rate is $32 per direct labor hour (= $8,000,000 ÷ 250,000 direct labor hours). Thus, as shown in Figure 3.1 “Using One Plantwide Rate to Allocate SailRite Company’s Overhead”, products are charged $32 in overhead costs for each direct labor hour worked.

How do you calculate applied overhead?

Apply overhead. Multiply the overhead allocation rate by the number of direct labor hours needed to make each product. Suppose a department at Band Book actually worked 20 hours on a product. Apply 20 hours x $25 = $500 worth of overhead to this product.

Why are direct labor hours and machine hours commonly used as the basis for overhead allocation?

The more direct labor hours worked, the higher the overhead costs incurred. Thus direct labor hours or direct labor costs would be used as the allocation base. If a company’s production process is highly mechanized (i.e., it relies on machinery more than on labor), overhead costs are likely driven by machine hours.

What is the amount of applied overhead?

The percentage of overhead that is applied to a given department may or may not correlate to the actual amount of overhead that was incurred by that department. Applied overhead costs include any cost that cannot be directly assigned to a cost object, such as rent, administrative staff compensation, and insurance.

How do you calculate overhead burden rate?

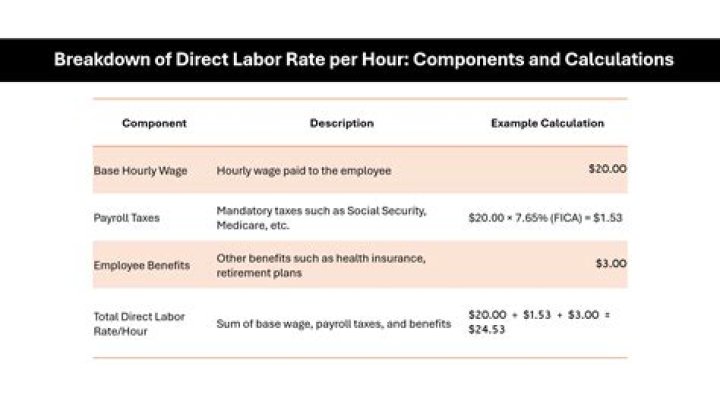

The burden rate is the dollar amount of burden (i.e., overhead) that is applied to one dollar of wages. For example, if the annual benefits and payroll taxes associated with an individual is $20,000 and his wages are $80,000, then the burden rate is $0.25 per $1.00 of wages.

Why do we calculate applied overhead?

Managerial Decision Making: As the total cost of the product is ascertained, including applied overhead cost, it helps in managerial decision making, i.e., pricing decisions if it can go with the production of a particular product.

What is the difference between actual and applied overhead?

In short, the main difference between the two concepts is that actual overhead is the amount of cost actually incurred, while applied overhead is the standard amount of overhead applied to cost objects.

What is the applied overhead based on direct labor hours?

You may also calculate the overhead rate based on direct labor hours. Divide the overhead costs by the direct labor hours over the same measurement period. In the example, the overhead rate is $20 for each direct labor hour ($2,000/100).

How do you calculate overhead per hour?

Most of the time, software companies calculate overhead costs by taking the total number of billable hours in all projects in a given period and divide their total overhead costs by that number. This is how they get the overhead rate per hour.

Does overhead include direct labor?

Overhead expenses are all costs on the income statement except for direct labor, direct materials, and direct expenses. Overhead expenses include accounting fees, advertising, insurance, interest, legal fees, labor burden, rent, repairs, supplies, taxes, telephone bills, travel expenditures, and utilities.

Is a receptionist direct labor or overhead?

Receptionist as it is not a direct Labour. It comes in the category of indirect labour because Indirect labor includes all the other wages and salaries paid to people who work in the production of the product but who are not touch or direct labor. Business loan is not a manufacturing overhead.

Which is better overhead absorption or direct labor cost?

This is considered as a better method for overhead absorption than direct labor cost method as is only based on time factor and is not distorted by factors like varying wage rates, overtime or bonus payments.

Is there relationship between labor cost and factory overheads?

This is recommended as unlike material prices; labor rates are relatively stable moreover there is direct relationship between direct labor cost and factory overheads on the basis that both are related to time.

How to calculate a business’s overhead absorption rate?

The use of this method requires a record of the direct labor hours expended on each job, product or cost unit in order to determine the share of overhead, it should bear. This method is more appropriate in a capital intensive cost center where use of machines is the most significant factor in production.

Why do you use machine hour rate for overhead absorption?

In such a cost center most of the production overheads are related to the machinery (power, repairs, depreciation, etc.), so a machine hour rate should reflect fairly the incidence of overheads. This is used as follows: