How do you calculate nominal risk-free rate?

James Williams

Published Feb 16, 2026

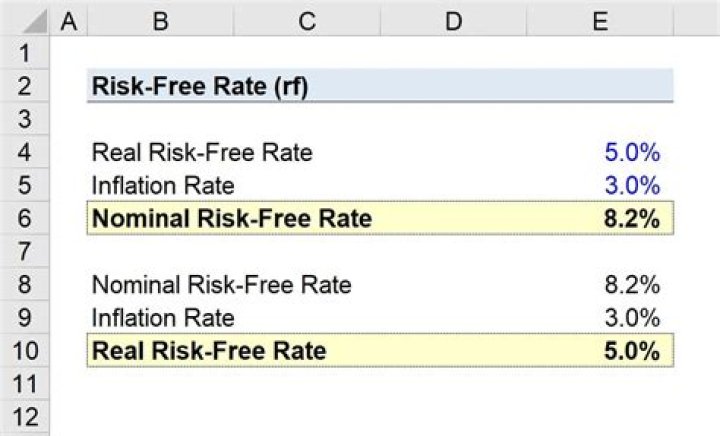

Nominal Risk Free Rate = (1 + Real Risk Free Rate) / (1 + Inflation Rate)

- Risk Free Rate = (1 + 2.5%) / (1 + 1%)

- Risk Free Rate = 1.01%

What is risk free security?

A security which is free of the various possible sources of risk. One is the risk that the debtor may default; this is thought to be absent in the case of UK, US, and many other countries’ government debt. In money terms, a government obligation is risk-free if the holder has the option to have it redeemed at any time.

Is it true that a US Treasury security is risk-free?

U.S. Treasuries are indeed risk-free for individuals who hold individual bonds until maturity. For those who sell their bonds before maturity or invest in long-dated Treasury funds, there is a risk.

What is a nominal annual interest rate?

The nominal interest rate, also known as an Annualised Percentage Rate or APR, is the periodic interest rate multiplied by the number of periods per year. For example, a nominal annual interest rate of 12% based on monthly compounding means a 1% interest rate per month (compounded).

Is risk-free rate real or nominal?

The real rate of interest is the nominal rate minus the expected inflation rate. However, the real rate itself has several components. First is the risk-free rate investors expect. This is the real rate you get on securities with negligible risk, like U.S. Treasury bonds.

What is the nominal risk-free rate rRF )? What securities can be used as estimates of rRF?

j. Define the nominal risk-free rate (rRF). What security can be used as an estimate of rRF The nominal risk-free rate, rRF, is equal to the real risk-free rate plus an inflation premium whichis equal to the average rate of inflation expected over the life of the security.

What is real and nominal interest rate?

A real interest rate is an interest rate that has been adjusted to remove the effects of inflation to reflect the real cost of funds to the borrower and the real yield to the lender or to an investor. A nominal interest rate refers to the interest rate before taking inflation into account.

What is the nominal interest rate formula?

The equation that links nominal and real interest rates can be approximated as nominal rate = real interest rate + inflation rate, or nominal rate – inflation rate = real interest rate.

How do you determine risk-free rate?

The value of a risk-free rate is calculated by subtracting the current inflation rate from the total yield of the treasury bond matching the investment duration. For example, the Treasury Bond yields 2% for 10 years. Then, the investor would need to consider 2% as the risk-free rate of return.

How to calculate the nominal risk free rate?

Nominal Risk Free Rate. = (1 + Real Risk Free Rate) × (1 + Inflation Rate) − 1. Where r f is the real risk-free rate and i is the relevant inflation rate.

What is the real risk free interest rate?

You estimate the cost of equity using the capital asset pricing model. The cash flows are in real terms, the nominal risk-free rate for the short-term Japanese government bills is 1.5%, the 10-year government bonds rate is 2.5% and inflation rate is 0.7%. US short-term and long-term treasury rates are 1.50% and 2.77% and the inflation rate is 1%.

How is risk free rate related to cost of capital?

Risk free rate is the key input in estimation of cost of capital. The capital asset pricing model estimates required rate of return on equity based on how risky that investment is when compared to a totally risk-free asset. Cost of debt is estimated by adding spreads for different risk premia to the risk-free rate.

What is the real risk free rate in Japan?

The cash flows are in real terms, the nominal risk-free rate for the short-term Japanese government bills is 1.5%, the 10-year government bonds rate is 2.5% and inflation rate is 0.7%.