How do you calculate net income under cash-basis?

Sarah Duran

Published Feb 18, 2026

Under the cash-basis method, you may not record any expenses that you have been billed for but have not paid. Subtract your total cash-basis expenses from your cash-basis income. The result is your net income using the cash -basis accounting method.

How do you do a cash-basis income statement?

Subtract any billings for which cash was received from customers. Subtract any cash deposits received from customers that have not been earned. Add billings to customers during the period. Add earned but unbilled products/services.

How do you calculate cash-basis and accrual basis?

How to convert cash basis to accrual basis accounting

- Add accrued expenses. Add back all expenses for which the company has received a benefit but has not yet paid the supplier or employee.

- Subtract cash payments.

- Add prepaid expenses.

- Add accounts receivable.

- Subtract cash receipts.

- Subtract customer prepayments.

What is cash basis net income?

Cash basis refers to a major accounting method that recognizes revenues and expenses at the time cash is received or paid out. This contrasts accrual accounting, which recognizes income at the time the revenue is earned and records expenses when liabilities are incurred regardless of when cash is received or paid. Live.

Is P&L cash or accrual?

Under accrual accounting, a business reports revenues and expenses when they are earned or incurred, regardless of when cash payment occurs. The profit or loss a company reports on its cash-basis P&L typically differs from the profit or loss calculated on an accrual basis.

How do you convert cash basis?

To convert from accrual basis to cash basis accounting, follow these steps:

- Subtract accrued expenses.

- Subtract accounts receivable.

- Subtract accounts payable.

- Shift prior period sales.

- Shift customer prepayments.

- Shift prepayments to suppliers.

How do I convert accrual books to cash?

How do you convert cash-basis to net income?

What is cash-basis income?

Cash basis refers to a major accounting method that recognizes revenues and expenses at the time cash is received or paid out. This contrasts accrual accounting, which recognizes income at the time the revenue is earned and records expenses when liabilities are incurred regardless of when cash is received or paid.

What is cash-basis P&L?

Cash-basis profit and loss equals a company’s cash received from sales minus its cash expenses during an accounting period. A company reports its sales, expenses and cash-basis profit or loss on its profit and loss statement, which is also known as a P&L or an income statement.

P&L. Under the cash method, income is only recorded if the money is actually received. Similarly, expenses are recorded only if cash really left the bank account. In contrast, the accrual method of accounting records income in the period it was earned, and expenses in the period in which they were incurred.

How to calculate net income on a cash basis?

For example, a carpenter who contracts a job for $2,000 and estimates his expenses to be $1,200, would also estimate his profit to be $800, or $2,000 minus $1,200. If he completes the project on December 23, 2011, but does not receive payment until January 3, 2012, his net loss for the year is $1,200, or $2,000 minus $800.

How are expenses recorded on a cash basis?

When using cash-basis income accounting, expenses required for a project or service are recorded as work is performed. Revenue, however, is not recorded until work is completed.

Why is it important to use cash basis?

Therefore, a cash-basis accounting method may reduce your liability one year, but increase it the next. A corporation that reports a net loss for the year may face a a lower stock price, as well as criticism from shareholders and potential investors.

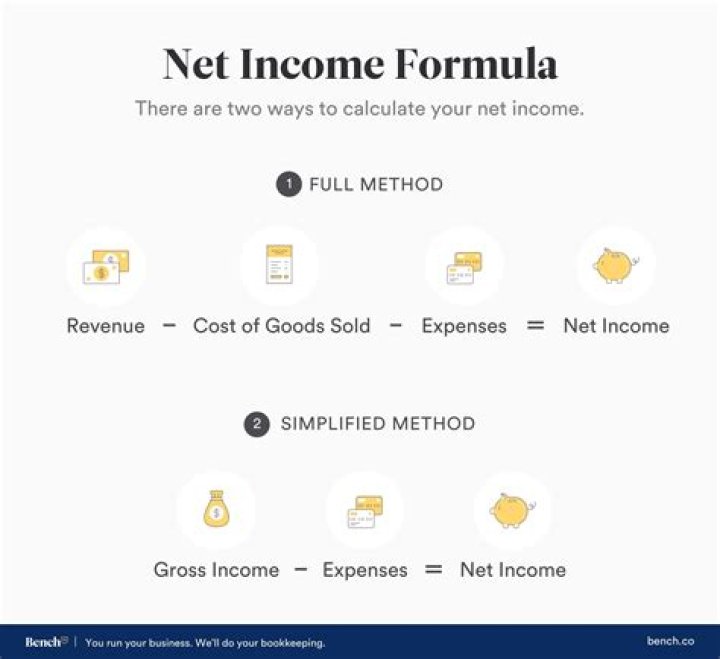

How is the net income of a company calculated?

Net income is calculated as revenues plus gains, minus expenses and losses. Revenue is income received from sales or services, while gains include transactions such as the proceeds from the sale of a company car. Expenses are those required for operation, such as rent and loan interest payments.