How do you calculate lower of cost or market?

Emma Jordan

Published Feb 18, 2026

Valuing Inventory at Lower of Cost or Market (LCM)

- Replacement cost > net realizable value, use net realizable value for replacement cost.

- Replacement cost < net realizable value minus a normal profit margin, use net realizable value minus a profit margin for replacement cost.

What is the lower cost method?

Understanding Lower of Cost or Market Method The lower of cost or market method lets companies record losses by writing down the value of the affected inventory items. The amount by which the inventory item was written down is recorded under cost of goods sold on the balance sheet.

How is the lower of cost or market rule applied when there are more than 2 types of inventory?

How is the lower-of-cost-or-market rule applied when there are more than 2 types of inventory? Only the items that have market values lower than the costs will be written down. Sales Revenue on the income statement and Accounts Receivable on the balance sheet.

When reporting inventory using the lower of cost or market method market should not be more than?

When reporting inventory using the lower of cost or market, market should not be less than: Net realizable value less a normal profit margin. The gross profit method can be used in all of the following situations except: In the preparation of annual financial statements.

What is the lower of cost and net realizable value rule?

The lower of cost or net realizable value concept means that inventory should be reported at the lower of its cost or the amount at which it can be sold. The loss appears within the cost of goods sold line item in the income statement. …

How do you calculate replacement cost?

Replacement Cost Value Calculator – the RCV Formula The most straightforward RCV calculation formula for estimating your home’s replacement cost value is to multiply your home’s square footage by the average square foot cost to rebuild a home in your area.

How the lower of cost is applied?

The lower of cost or market rule states that a business must record the cost of inventory at whichever cost is lower – the original cost or its current market price.

What is the LCM rule?

The lower of cost or market (LCM) method states that when valuing a company’s inventory, it is recorded on the balance sheet at either the historical cost or the market value. Historical cost refers to the cost at which the inventory was purchased. The value of a good can shift over time.

How do you calculate NRV per unit?

Subtract the costs required to prepare the item for sale from the expected selling price. The result is the net realizable value of the item in inventory. Add up the NRV for all items, and the result is the total net realizable value for the company’s inventory.

How does the lower of cost method work?

The lower of cost or market method states that when valuing a company’s inventory, it is recorded on the balance sheet at either the historical cost or the market value. Historical cost is the cost at which the inventory was purchased. However, the value of a good can change.

What does lower of cost or market mean?

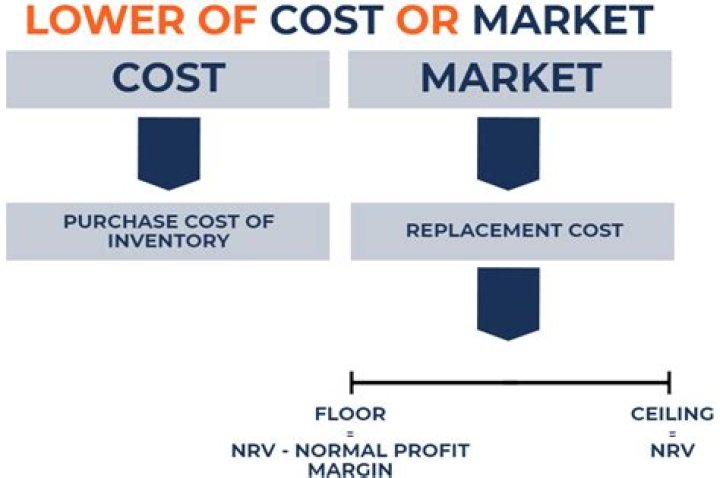

Lower of cost or market (LCM) is an inventory valuation method required for companies that follow U.S. GAAP. Cost refers to the purchase cost of inventory, and market value refers to the replacement cost of inventory. The replacement cost cannot exceed the net realizable value or be lower than the net realizable value less a normal profit margin.

How to calculate lower of cost or market ( LCM )?

1 First, determine the historical purchase cost of inventory. 2 Second, determine the replacement cost of inventory. It is the same as the market value of inventory. 3 Compare replacement cost to net realizable value and net realizable value minus a normal profit margin. 4 Compare the cost of inventory to replacement cost. Lastly, if:

When to use the lower of cost rule?

Lower of Cost or Market Overview. The lower of cost or market rule states that a business must record the cost of inventory at whichever cost is lower – the original cost or its current market price. This situation typically arises when inventory has deteriorated, or has become obsolete, or market prices have declined.