How do you allocate direct labor costs?

John Thompson

Published Feb 20, 2026

The labor cost per unit is obtained by multiplying the direct labor hourly rate by the time required to complete one unit of a product. For example, if the hourly rate is $16.75, and it takes 0.1 hours to manufacture one unit of a product, the direct labor cost per unit equals $1.68 ($16.75 x 0.1).

Why might a company use direct labor cost as an overhead allocation base rather than using direct labor hours?

The more direct labor hours worked, the higher the overhead costs incurred. Thus direct labor hours or direct labor costs would be used as the allocation base. If a company’s production process is highly mechanized (i.e., it relies on machinery more than on labor), overhead costs are likely driven by machine hours.

How is direct labor cost allocated overhead?

How to Calculate Overhead Allocation

- Add up total overhead.

- Compute the overhead allocation rate by dividing total overhead by the number of direct labor hours.

- Apply overhead by multiplying the overhead allocation rate by the number of direct labor hours needed to make each product.

Which is the best method for allocating overhead cost?

The best method for allocating overhead in construction is a way that’s fair. After all, the idea is to allocate (or, distribute) costs that each job shares responsibility for — meaning the job either caused or benefited from the cost. But, the costs should also be proportional to that responsibility.

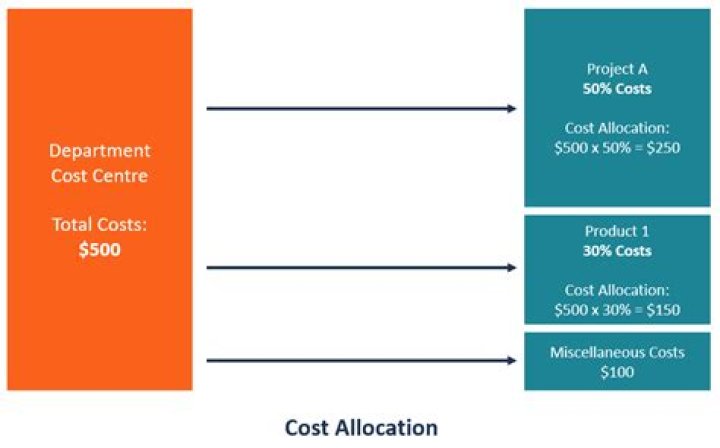

How to calculate Cost allocation of direct labor?

After determining that direct labor hours will be used as the cost driver to allocate indirect costs, you can divide total indirect costs in the cost pool by total direct labor hours. This will give you an overhead rate per direct labor hour.

How does a company use a cost allocation basis?

A company usually uses a single cost allocation basis, such as labor hours or machine hours, to allocate costs from cost pools to designated cost objects. A company with a cost pool of manufacturing overhead uses direct labor hours as its cost allocation basis.

How is overhead allocated in a cost structure?

A company with a cost pool of manufacturing overhead uses direct labor hours as its cost allocation basis. The company first accumulates its overhead expenses over a period of time, say for a year, and then divides the total overhead cost by the total number of labor hours to find out the overhead cost “per labor hour” (the allocation rate).

How are indirect costs allocated in a business?

The indirect costs must be pooled and allocated by calculating an overhead rate. Sales revenue minus manufacturing costs — called cost of goods sold — equals gross profit. Manufacturing costs can be separated into direct materials, direct labor and manufacturing overhead.