How do you account for disposal?

Emma Jordan

Published Feb 17, 2026

Debit the cash account for any proceeds from the sale, and credit the disposal account. Debit the disposal account if there is a loss on disposal. Credit the fixed asset account to reverse the original cost of the asset, and debit the disposal account. Credit the disposal account if there is a gain on disposal.

How do you record equipment acquisition?

To record purchase of equipment by paying cash and signing note. Sometimes a company buys land and other assets for a lump sum. When land and buildings purchased together are to be used, the firm divides the total cost and establishes separate ledger accounts for land and for buildings.

How do you record an asset acquisition?

Acquisition: Accounting for Purchase of Fixed Assets. To record the purchase of a fixed asset, debit the asset account for the purchase price, and credit the cash account for the same amount.

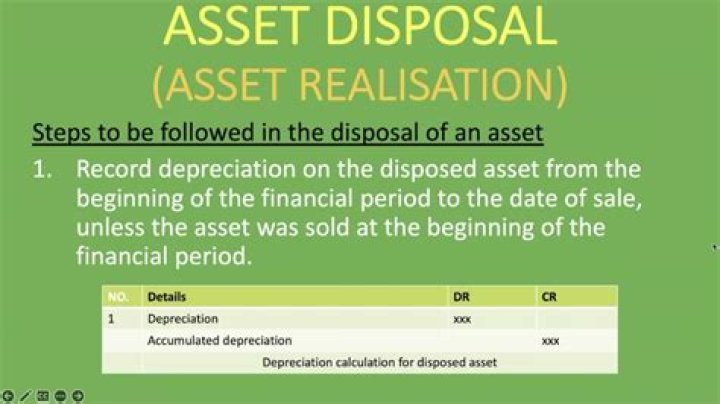

How are disposals of plant assets accounted for?

Disposal of plant assets Bring the asset’s depreciation up to date. Record the disposal by: Writing off the asset’s cost. Writing off the accumulated depreciation.

Is disposal account an expense?

if there is a credit entry to balance the account then this is a loss on disposal which is debited to the SPL as an additional expense. There is an alternative to selling a non-current asset for cash, particularly if a new asset is to be purchased to replace the one being sold.

What is the journal entry for selling an asset?

Debit cash for the amount received, debit all accumulated depreciation, debit the loss on sale of asset account, and credit the fixed asset. Gain on sale. Debit cash for the amount received, debit all accumulated depreciation, credit the fixed asset, and credit the gain on sale of asset account.

What is a disposal in accounting?

The disposal account is the account which is used to make all of the entries relating to the sale of the asset and also determines the profit or loss on disposal. 1.3 Profit or loss on disposal. The value that the non-current is recorded at in the books of the.

How do you treat land in accounting?

Unlike a majority of fixed assets, land is not subject to depreciation. Land is listed on the balance sheet under the section for non-current assets. Increases in market value are disregarded on the balance sheet.

How do you record a journal entry for sale of inventory?

So a typical sales journal entry debits the accounts receivable account for the sale price and credits revenue account for the sales price. Cost of goods sold is debited for the price the company paid for the inventory and the inventory account is credited for the same price.

How do you record goodwill journal entries?

If the goodwill account needs to be impaired, an entry is needed in the general journal. To record the entry, credit Loss on Impairment for the impairment amount and debit Goodwill for the same amount. This accounts for a reduction in Goodwill by using Loss on Impairment as a contra-asset account.