How do you account for building depreciation?

John Thompson

Published Mar 22, 2026

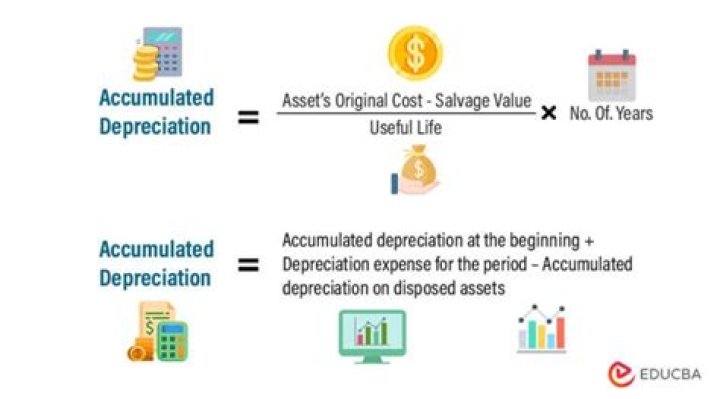

Each year that you depreciate a building, you debit the amount to Depreciation Expense. You also credit the same figure to Accumulated Depreciation. The figure in the latter account increases over time as annual depreciation adds up.

What is the useful life of a building for depreciation?

Buildings are generally depreciated over a 27.5 or 39 year life and bonus depreciation only applies to assets with a recovery period of 20 years or less.

How do you determine the useful life of a building?

How to determine the useful life of an asset. Most commonly, the depreciation of assets is calculated by dividing the cost of the asset by the estimated number of years in its life.

How do you find the depreciation value of a building?

You can use the property tax assessor’s values to compute a ratio of the value of the land to the building. Multiply the purchase price ($100,000) by 25% to get a land value of $25,000. You can depreciate your $75,000 basis in the building using the mid-month MACRS tables.

What is economic life of a building?

Economic life is the expected period of time during which an asset remains useful to the average owner. When an asset is no longer useful to its owner, then it is said to be past its economic life. The economic life of an asset could be different than its actual physical life.

Can I depreciate my office building?

Commercial and residential building assets can be depreciated either over 39-year straight-line for commercial property, or a 27.5-year straight line for residential property as dictated by the current U.S. Tax Code.

Do you depreciate buildings held for sale?

Once an asset is held for sale, it is no longer depreciated.

How do you account for buildings?

Buildings is a noncurrent or long-term asset account which shows the cost of a building (excluding the cost of the land). Buildings will be depreciated over their useful lives by debiting the income statement account Depreciation Expense and crediting the balance sheet account Accumulated Depreciation.

When do you have to depreciate land and buildings?

If the property is classified as “property, plant and equipment (PPE)” land is there not depreciated but the buildings are. When land, however, is used as a quarry, under exceptional cases, it shall be depreciated because the land is going to be depleted over time. Buildings are therefore depreciated, just as in the case of other PPE items.

Who is the best person to depreciate a building?

For best results, use a quantity surveyor who is a depreciation specialist and registered tax agent. Commercial building construction costs and assets can be substantially different to those we see for residential homes, and a specialist will understand the commercial scale of the building, and the industry specialised assets.

Can a fully depreciated asset be revalued?

A fully depreciated asset cannot be revalued because of accounting’s cost principle. A fully depreciated asset is one that has accumulated depreciation equal to its cost.

Why are machines fully depreciated but we still use them?

None, of course – because the carrying amount of your property, plant and equipment cannot decrease below zero. So in fact, you use the machines, but you can’t really recognize any depreciation expense, because there’s nothing left. You have fully depreciated these assets in the previous reporting periods.