How do you account for acquisition on a balance sheet?

Ava Robinson

Published Feb 10, 2026

On the date of acquisition, goodwill arising from the business combination should be recognized in the balance sheet of the acquirer as an intangible asset. The asset is measured as the excess of the acquisition cost over the acquirer’s interest in the fair value of the assets acquired and the liabilities assumed.

Where do acquisitions go on the balance sheet?

Under standard accounting rules, any costs you incurred to carry out the acquisition are considered part of the purchase price, according to Corporate Finance Institute. As such, they go on the balance sheet as capitalized costs, not on the income statement as expenses.

How do you account for an asset acquisition?

For an asset acquisition that is within the scope of ASC 805-50, if the consideration given includes noncash assets, liabilities incurred, or equity interests issued, the assets acquired are measured by using either the cost to the acquiring entity or the fair value of the net assets acquired, whichever is more …

Is an acquisition an expense?

The cost of acquisition is the total expense incurred by a business in acquiring a new client or purchasing an asset. An accountant will list a company’s cost of acquisition as the total after any discounts are added and any closing costs are deducted.

What is gain on acquisition?

An acquirer must record the difference between the purchase price and fair value as a gain on the balance sheet as negative goodwill. The difference in the price paid and fair value is recorded as a gain.

How are acquisitions accounted for?

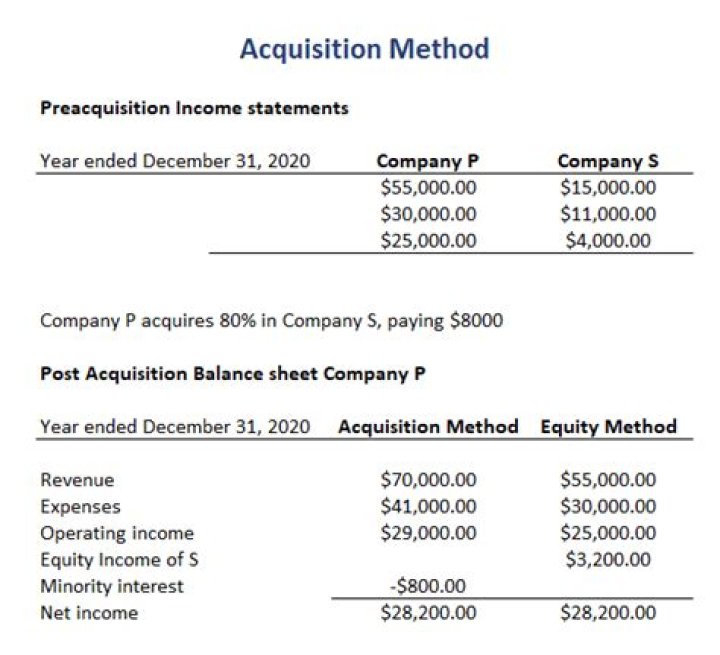

Acquisition accounting is a set of formal guidelines describing how assets, liabilities, non-controlling interest (NCI) and goodwill of a purchased company must be reported by the buyer on its consolidated statement of financial position. Acquisition accounting is also referred to as business combination accounting.

Can you have goodwill in an asset acquisition?

Goodwill is not recognized in an asset acquisition. Even if there is economic goodwill in the transaction, this amount is allocated to the assets acquired based on their relative fair values. This results in a higher asset basis that must then be amortized or depreciated.

When to make opening balance sheet adjustments at acquisition?

The fair market values – not the book values – of the assets acquired total $400,000. On the acquisition date, Company A adjusts its balance sheet by debiting various asset accounts for $400,000, debiting “Goodwill” for $100,000 and crediting “Cash” for $500,000. Company A may purchase half of the stock of Company B for $250,000 cash.

How are assets recorded in purchase acquisition accounting?

Purchase acquisition accounting is now the standard way to record the purchase of a company on the balance sheet of the acquiring company. The assets of the acquired company are recorded as assets of the acquirer at fair market value.

How are assets and liabilities organized on a balance sheet?

A balance sheet is organized into two sections.The first section lists all of the company’s assets. The second sections lists the firm’s liabilities and owner’s equity. The company’s total assets must equal the sum of the total liabilities and total owners equity; that is, the totals must balance.

Where does the opening balance equity account go?

Once all initial account balances have been entered, the balance in the opening balance equity account is moved to the normal equity accounts, such as common stock and retained earnings.