How do I report IRA distribution back?

Andrew Mclaughlin

Published Apr 05, 2026

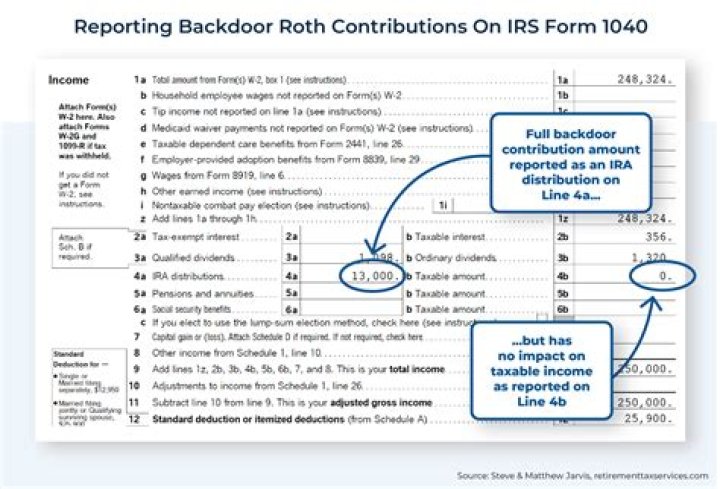

You will need to indicate a rollover on your tax return (that’s what returning an unwanted RMD is), and that is relatively easy. The total distribution from the IRA must be indicated on line 4a of Form 1040 when preparing your federal income tax return. Then, enter “rollover” next to line 4b.

To correctly report the distribution and rollover on Form 1040, the retiree must include the full amount of the distributions on line 4a. If the entire amount was rolled over, or returned, to the IRA, put zero on line 4b as the taxable amount.

Can a distribution be put back into an IRA?

But they also allow you to redeposit the money back into the existing IRA, acknowledging the fact that IRA accountholders will sometimes change their minds about a provider switch. As a result, if you can fit within the 60-day rollover window, you can simply redeposit the full amount of the distribution back into your IRA.

What happens when you put money back into an IRA?

If you put money back into your IRA that wasn’t eligible to be rolled over, you’re treated as having taken a distribution and made a separate contribution. The distribution becomes fully taxable and the contribution is subject to your annual contribution limits.

Can a rollover IRA be put back into an IRA?

If you take a distribution from a plan that has already been part of a rollover within the last 12 months, that money is ineligible to be put back into an IRA. You must report your IRA distributions and re-contributions on your income taxes even if you don’t incur any additional income tax liability.

Where does the amount of an IRA distribution go on a 1040?

Using the information on your 1099-R, you enter the amount of your total IRA distribution on line 4a of Form 1040. The taxable amount, which should be zero, goes on line 4b. You can generally rollover an IRA to another IRA without tax penalty.