How do I report a qualified Roth IRA distribution?

Sarah Duran

Published Apr 01, 2026

Tax Reporting for Qualified Distributions Even though qualified Roth IRA distributions aren’t taxable, you must still report them on your tax return using either Form 1040 or Form 1040A. If you opt to use Form 1040 to file your taxes, enter the nontaxable amount of your qualified distribution on line 15a.

What makes a Roth distribution qualified?

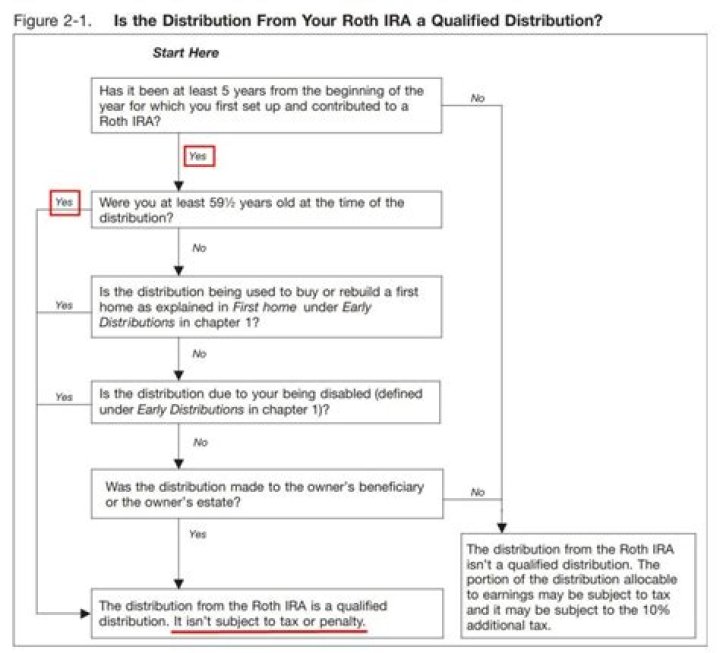

Any earnings you withdraw are considered “qualified distributions” if you’re 59½ or older, and the account is at least five years old, making them tax- and penalty-free.

Do qualified Roth distributions count as income?

Earnings from a Roth IRA don’t count as income as long as withdrawals are considered qualified. Typically, you need to be at least 59½ and the account at least five years old for a distribution to count as qualified, but there are exceptions.

Is there a 10% penalty on Roth conversions?

If you withdraw contributions before the five-year period is over, you might have to pay a 10% Roth IRA early withdrawal penalty. This is a penalty on the entire distribution. You usually pay the 10% penalty on the amount you converted. A separate five-year period applies to each conversion.

Any earnings you withdraw are considered “qualified distributions” if you’re 59½ or older, and the account is at least five years old, making them tax- and penalty-free. Other kinds of withdrawals are considered “non-qualified” and can result in both taxes and penalties.

When do you have to make a qualified distribution from a Roth IRA?

Roth IRA Qualified Distribution Explained Qualified distributions from a Roth IRA are done when a person is over 59.5 years old or meets some special qualifications. The IRS spells out the rulesfor Roth IRA qualified distributions. Generally, a distribution or withdrawal is considered to be qualified if it’s made at age 59.5 or later.

What does it mean to have a non qualified Roth IRA?

What Is a Non-Qualified Roth IRA Distribution? A non-qualified distribution from an Roth IRA is any distribution that doesn’t follow the guidelines for Roth IRA qualified distributions. Specifically, that means distribution: Taken before age 59.5. That don’t meet the five-year requirement. That don’t qualify for an exception.

What are the tax implications of a non qualified distribution?

The tax implications of a non-qualified distribution depend on the source of the Roth IRA assets. There are four possible sources of Roth IRA assets: Regular participant contributions and rollover of basis from designated Roth accounts.

How are contributions distributed in a Roth IRA?

Under the ordering rules applicable to Roth IRAs, contributions are always deemed to be withdrawn first. Roth conversion amounts are not considered distributed until all contribution amounts have been distributed; earnings are not considered distributed until all contribution—and then all conversion—amounts have been distributed.