How do I know if I will receive a 1099-R?

James Williams

Published Apr 07, 2026

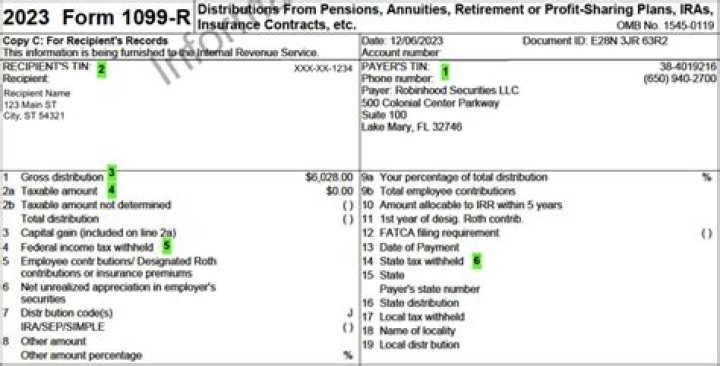

You should receive a copy of Form 1099-R, or some variation, if you received a distribution of $10 or more from your retirement plan. Form 1099-R is used to report the distribution of retirement benefits such as pensions, annuities or other retirement plans.

Why have I not received my 1099-R?

If you do not receive your Form W-2 or Form 1099-R by January 31st , or your information is incorrect, contact your employer/payer. If you do not receive the missing or corrected form by February 14th from your employer/payer, you may call the IRS at 1-800-829-1040 for assistance.

What do you need to know about Form 1099-R?

About Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. File this form for each person to whom you have made a designated distribution or are treated as having made a distribution of $10 or more from. profit-sharing or retirement plans,

When to file a 1099-R pension distribution?

About Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. File Form 1099-R for each person to whom you have made a designated distribution or are treated as having made a distribution of $10 or more from:

How long does it take for a 1099-R to arrive?

It may take up to 10 days for the form to arrive with mailing time, but if you do not receive your 1099-R by February 10th, please let us know so we can send you a new copy. When you receive your Form 1099-R, it’s important to remember that distributions from traditional 401(k) accounts are generally reportable on your income taxes.

When do I receive a 1099-R from an inherited IRA?

When a taxpayer receives a distribution from an inherited IRA, they should receive from the financial instruction a 1099-R, with a Distribution Code of ‘4’ in Box 7. This gross distribution is usually fully taxable to the beneficiary/taxpayer unless the deceased owner had made non-deductible contributions to the IRA.