How do I convert an LLC to a partnership?

Emma Jordan

Published Apr 03, 2026

In general, LLCs and LLPs share the same legal protection and tax benefits but an LLP can reduce a partner’s liability in some states.

- Review your state’s LLP laws.

- Contact the Internal Revenue Service.

- Dissolve your LLC.

- Create a Partnership Agreement.

- File your Articles of Organization or Formation.

How LLC partnerships are taxed?

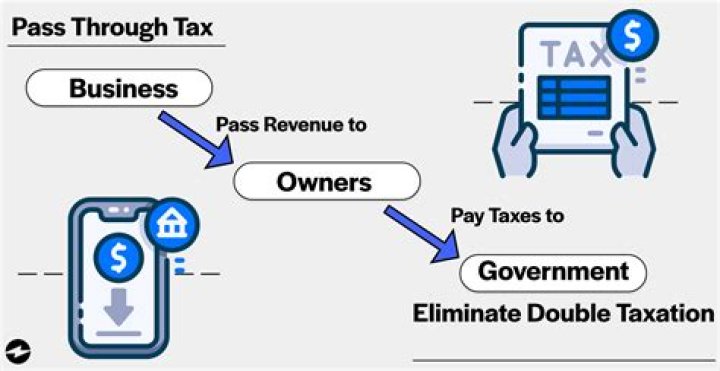

An LLC taxed as a partnership must provide a Schedule K-1 to each member, which will be included with their personal tax returns. The business doesn’t have to pay taxes directly. Instead, each business partner or member will report income and losses and pay income taxes based on their ownership share in the company.

What is a converted Out LLC?

Converted-Out: The business entity converted to another type of business entity or to the same type under a different jurisdiction as provided by statute. The name of the new entity can be obtained by ordering a copy of the filed conversion document containing the name of the new entity, or by ordering a status report.

When to convert a single member LLC to a multi member LLC?

Converting a single-member LLC to multi-member LLC occurs when the ownership stake of a limited liability company is divided among additional owners, referred to as “members.” LLCs are a common organizational structure for small businesses because of their flexible management structure and ease of establishment.

Can a LLC be converted to a partnership?

The taxpayer to which the ruling was issued asked the IRS to consider whether the conversion of a State law limited liability company (“LLC”) into a State law limited partnership would cause the LLC or its members to recognize taxable income or gain. Now, some of you may say, “big whoop.” (I did say the result was obvious.)

Who is the sole member of LLC 2?

Corp-2 was classified as a corporation for tax purposes, and was the sole member of LLC-2; thus, Corp-2 was treated as the second member of LLC-1 for tax purposes. The other membership interests in LLC-1 were non-managing member interests owned either indirectly by Corp-2 (including through subsidiaries of LLC-2), or by other investors.

Are there gains or losses on a LLC conversion?

Taxability of Transaction: There is no gain or loss recognized by A or B as a result of converting a disregarded entity into a partnership. However, A may be required to recognize a gain on the sale of the LLC interest to B; to the extent the purchase price exceeds A ’s basis in the assets being treated as sold.