How do I calculate AMT depreciation?

Sarah Duran

Published Feb 28, 2026

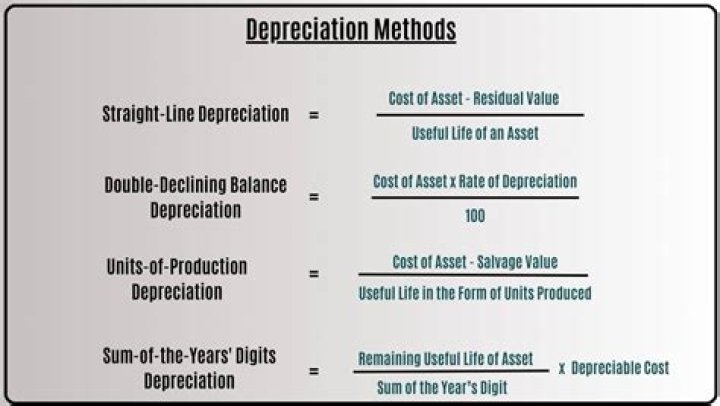

The straight-line method of depreciation spreads the cost of the asset, less the residual value of the asset, evenly across each period of the useful life of the asset. Subtract the depreciation calculated using the straight-line method from the depreciation calculated using any other method.

How is AMT tax calculated?

The AMT exemption amount for certain individuals under 24 equals their earned income plus $7,900. Multiply what’s left by the appropriate AMT tax rates. The AMT has two tax rates: 26% and 28%. (Compare these to the seven federal income tax brackets, ranging from 10% to 37%.)

Can Post 1986 depreciation adjustment be negative?

NOTE: See the instructions for Form 6251, under the heading “Post-1986 Depreciation” for more information on the specific differences in the calculation of regular tax and AMT depreciation. Because basis may be higher or lower for regular tax than it is for AMT, this adjustment may be positive or negative.

What are AMT depreciation adjustments?

The AMT depreciation adjustment for IRC Section 1250 property placed in service after 1986 and before 1999 is the difference between what was claimed for regular income tax and what was allowed under MACRS ADS SL depreciation.

How to find the post 1986 depreciation adjustment?

Line 17A – Post-1986 Depreciation Adjustment – This amount represents the taxpayer’s post-1986 depreciation adjustment. This amount will automatically pull to line 2i of Form 6251. Line 17B – Adjusted Gain or Loss – This amount represents the taxpayer’s adjusted gain or loss. This amount will automatically pull to line 2k of Form 6251.

How to calculate depreciation for a first year home?

To find the depreciation value for the first year, use the following formula: (net book value – salvage value) x (depreciation rate). The depreciation for year one is $2,000 ($5000 – $1000 x 0.5).

How is depreciation calculated for last year of useful life?

In the final year, the depreciation for the last year of the useful life is calculated with this formula: (net book value at the start of year three) – (estimated salvage value). In this case, the depreciation expense is $1,000 in the final year.

When does the IRS publish Publication 946 for depreciation?

Much of it comes directly from IRS Publication 946. A special note about automobile depreciation. In February 2019, the IRS published a revenue procedure that “provides a safe harbor method of accounting for determining depreciation deductions for passenger automobiles.”