How can Accumulated depreciation be properly described?

John Thompson

Published Apr 04, 2026

Accumulated depreciation is the sum of all recorded depreciation on an asset to a specific date. Accumulated depreciation is presented on the balance sheet just below the related capital asset line. The carrying value of an asset is its historical cost minus accumulated depreciation.

Why is accumulated depreciation a credit?

Accumulated depreciation has a credit balance, because it aggregates the amount of depreciation expense charged against a fixed asset. This account is paired with the fixed assets line item on the balance sheet, so that the combined total of the two accounts reveals the remaining book value of the fixed assets.

How do you deal with accumulated depreciation?

If you take the original the cost of the asset (your purchase price), and subtract the accumulated depreciation, you get the “book value” or the “carrying value” of the asset. Accumulated depreciation is known as a “contra-asset”. This means that accumulated depreciation is an asset account with a credit balance.

How does Accumulated depreciation go down?

A decrease in accumulated depreciation will occur when an asset is sold, scrapped, or retired. At that point, the asset’s accumulated depreciation and its cost are removed from the accounts.

Why would you debit accumulated depreciation?

When you record depreciation on a tangible asset, you debit depreciation expense and credit accumulated depreciation for the same amount. This shows the asset’s net book value on the balance sheet and allows you to see how much of an asset has been written off and get an idea of its remaining useful life.

Is Accumulated depreciation a revenue?

Accumulated depreciation is the cumulative depreciation over an asset’s life. In accounting, accumulated depreciation is recorded as a credit over the asset’s useful life. When an asset is sold or retired, accumulated depreciation is marked as a debit against the asset’s credit value. It does not impact net income.

How does accumulated depreciation affect the value of an asset?

since the asset was put into use. It is a contra-asset account – a negative asset account that offsets the balance in the asset account it is normally associated with. Unlike a normal asset account, a credit to a contra-asset account increases its value while a debit decreases its value.

How much is accumulated depreciation on a contra asset?

Each year the contra asset account referred to as accumulated depreciation increases by $10,000. For example, at the end of five years, the annual depreciation expense is still $10,000, but accumulated depreciation has grown to $50,000.

When does accumulated depreciation need to be zeroed out?

For example, let’s say an asset has been used for 5 years and has an accumulated depreciation of $100,000 in total. After the 5-year period, if the company were to sell the asset, the account would need to be zeroed out because the asset is not relevant to the company anymore.

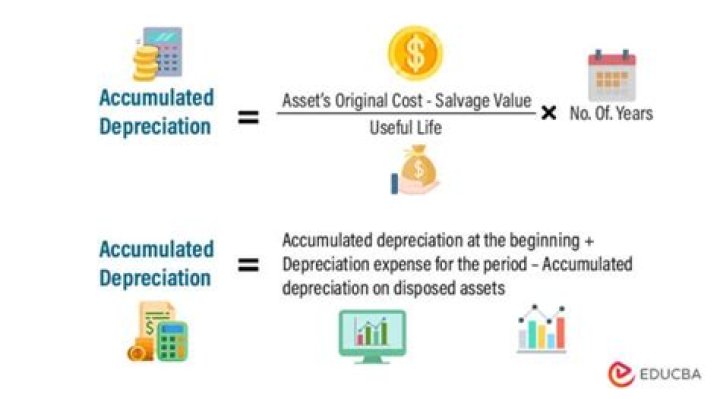

How to calculate accumulated depreciation expenses for 2019?

See the example of accumulated depreciation expenses below: let say the opening balance of accumulated depreciation at the 1st Jan 2019 is USD400,000 and the depreciation charge in the year 2019 is USD40,000, then the entries are as following: Dr_Depreciation expenses 40,000 (P&L) Cr_Accumulated depreciation 40,000 (BS)