How are short term capital losses taxed?

John Thompson

Published Feb 20, 2026

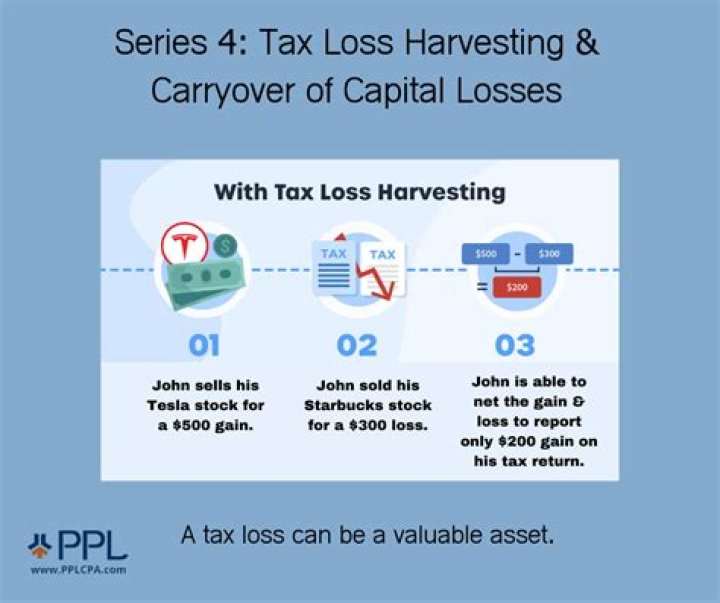

According to the tax code, short- and long-term losses must be used first to offset gains of the same type. The tax code allows joint filers to apply up to $3,000 a year in capital losses to reduce ordinary income, which is taxed at the same rate as short-term capital gains.

How do you calculate capital loss?

Capital Loss = Purchase Price – Sale Price If the sale price is higher than the purchase price, it is referred to as a capital gain.

How long can you carry over short term capital losses?

Capital Losses A net capital loss is carried back 3 years and forward up to 5 years as a short-term capital loss.

How far can you carry forward capital losses?

Key Takeaways

- Capital losses that exceed capital gains in a year may be used to offset ordinary taxable income up to $3,000 in any one tax year.

- Net capital losses in excess of $3,000 can be carried forward indefinitely until the amount is exhausted.

How long can you carry forward capital losses?

Capital losses that exceed capital gains in a year may be used to offset ordinary taxable income up to $3,000 in any one tax year. Net capital losses in excess of $3,000 can be carried forward indefinitely until the amount is exhausted.

How many years can you carry capital losses forward?

For a corporation, capital losses are allowed in the current tax year only to the extent of capital gains. A net capital loss is carried back 3 years and forward up to 5 years as a short-term capital loss.

How many years can you carry forward long term capital losses?

How long can you carry forward a net operating loss?

Section 2303 of the CARES Act amended section 172 as revised by the Tax Cuts and Jobs Act (TCJA), section 13302, for tax years 2018, 2019, and 2020. Taxpayers can carry back NOLs, including non-farm NOLs, arising from tax years beginning in 2018, 2019, and 2020 for 5 years.

How much loss can you carry forward?

Carrying Losses Forward You can use a maximum of $3,000 of capital losses each year as a write-off against income other than capital gains. If your losses are greater than your gains by more than $3,000, the extra losses above the $3,000 limit can be carried forward to future tax years.

Which losses Cannot be carried forward?

The following losses cannot be carried forward unless the return of income (for the year in which the loss is incurred) is submitted within the due date [of submission of return as given in section 139(1)]. loss (not being unabsorbed depreciation etc., from the activity of owning and maintaining race horses.

How far can losses be carried back?

Basically, if a company has stopped trading, and during its last 12 months in operation it made a loss, it can carry back its trading losses and offset them against profits made at any point up to three years before the year in which the loss was made.

What are tax losses carried forward?

Carried-forward tax losses are offset first against any net exempt income and only then against assessable income. Losses must be claimed in the order in which they were incurred.